The national advocacy organization Justice in Aging recently called attention to the critical role that oral…

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/gWWH0IjSvCU

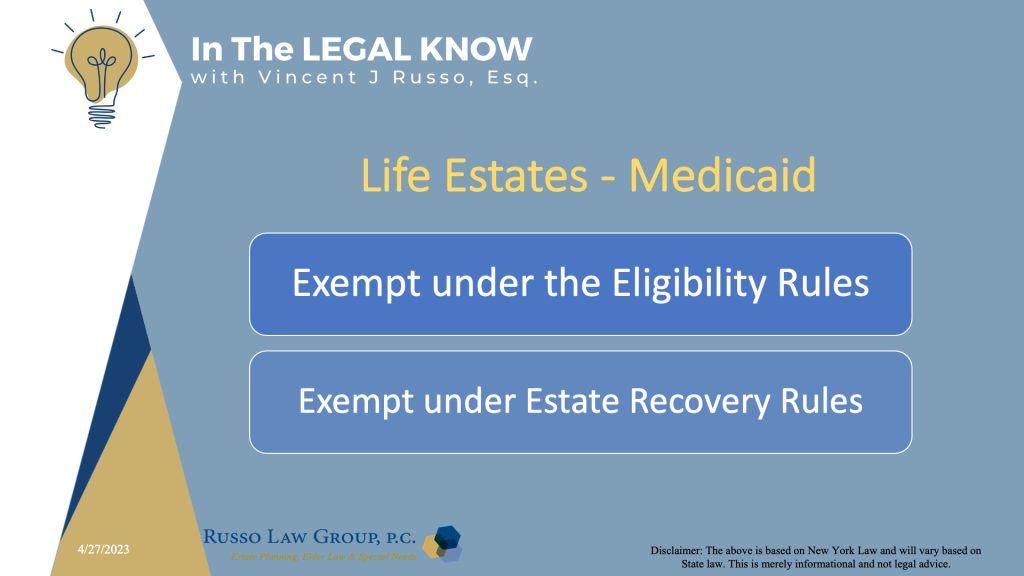

How does Medicaid treat life estates when it comes to Medicaid eligibility?

First, let’s explain two basic Medicaid rules when it comes to your primary residence. Under Medicaid, a primary residence is generally exempt under the Medicaid rules but not exempt from a potential Medicaid estate recovery. If one transfers their home and retains a life estate, there is no Medicaid estate recovery when the life tenant passes away.

A life estate interest is also exempt under the Medicaid Eligibility Rules and exempt under the Medicaid Estate Recovery Rules. So, life estates can be a useful Medicaid planning strategy.

For example, let’s say Mom owns her home and needs long term care but cannot afford to privately pay. She can transfer her home to her children and retain a life estate. She would be eligible for Medicaid home care under the current laws and when she passes, there would be no recovery by Medicaid against the home.

This strategy also preserves the STAR exemption for seniors who otherwise qualify and the step up in basis which can save capital gains taxes.

Is there a waiting period before Mom in your example can qualify for Medicaid?

It will depend; under current Medicaid home care rules, there is no waiting period. This is scheduled to change in July in New York but there is also a proposal not to implement a transfer waiting period for Medicaid home care. Stay tuned.

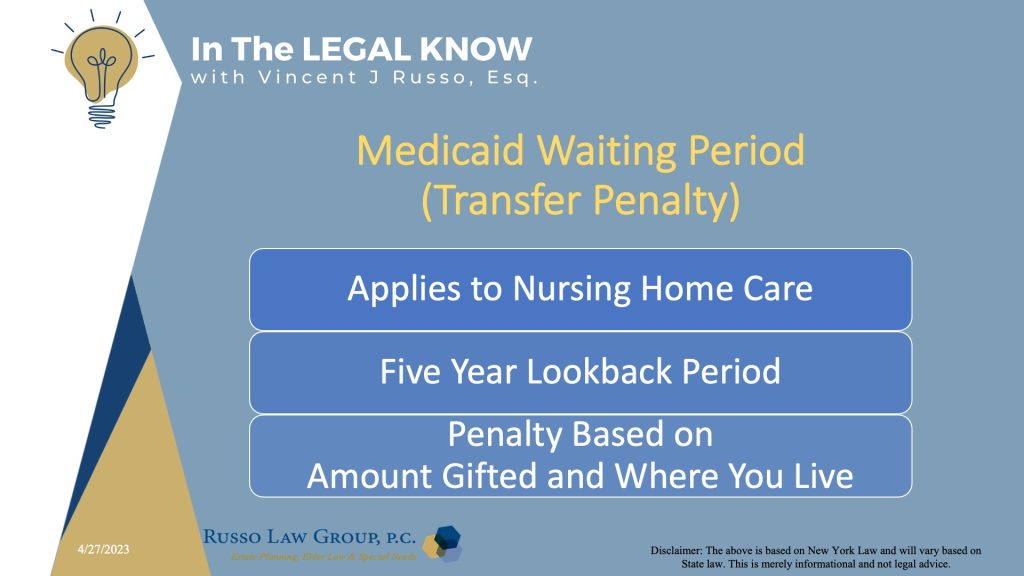

For nursing home care, there is a five year look back rule and a transfer penalty rule. So, there could be a waiting period if the transfer is made within the five years of applying for Medicaid. The Penalty is based on the amount of the gift and which county you live in.

The good news is that the transfer penalty or waiting period (the number of months you are not eligible for Medicaid) is shorter because mom in our example retained a life estate.

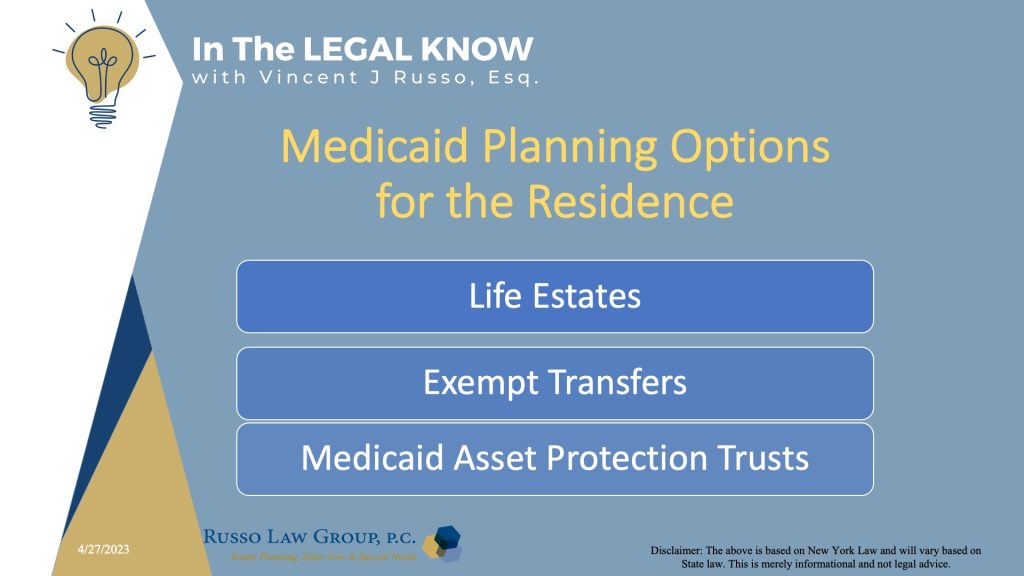

Is this strategy the best approach for protecting one’s home?

There is no one best strategy for protecting one’s home.

Life Estates are one option. Other options include exempt transfers to certain people and trusts that are not subject to a Medicaid transfer penalty and also the use of Medicaid Asset Protection Trusts. In many cases, we prefer the Medicaid Asset Protection Trust over the life estate strategy as more protections can be given when a trust is involved.

Once again, one should seek the counsel of an elder law attorney before using Life Estates in your estate plan: there are pros and cons to life estates, tax consequences and Medicaid implications.

Want to learn more about life estates?

Click here to read PART 1 and click here to read PART 2: TAXES

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Related Posts

Comments (0)