Understand the intricacies of tax return filings. Vincent J. Russo shares crucial insights to make filing easier.

The cost of nursing home care is staggering. With the average stay in a nursing home being 2.29 years, it is reported that as many as 80% of aging adults lack the financial resources to pay for that care. Therefore, seniors can lose all that they have in a crisis.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/vRwM-9IoUcE

Does Medicaid cover long term care?

Our broken health care system discriminates against seniors and people with disabilities who need long term care. Medicare does not cover long term care.

With nursing homes costing on average over $100,000 per year, this creates an acute financial crisis for many seniors. In New York, the cost rises to over $150,000 per year.

What government program covers long term care?

The only government program that will cover long term care is Medicaid. That program is a financially needs based program, so you have to be financially eligible to qualify. In many cases, planning becomes critical.

If I have assets in my name, will I qualify for Medicaid?

Depending on the state you reside in the rules will vary. For most states, once you have over $2,000 in assets (with certain exceptions) you will not be eligible for Medicaid. There are exceptions for certain assets such as your residence and personal property. Also, there is a different asset test if you are married which can provide greater protection.

As a general rule, if you transfer (gift) your assets away within five years of applying for Medicaid nursing home care (referred to as the lookback rule), then you will be penalized and not be eligible for coverage for a certain number of months. The period of ineligibility depends upon how much you transferred.

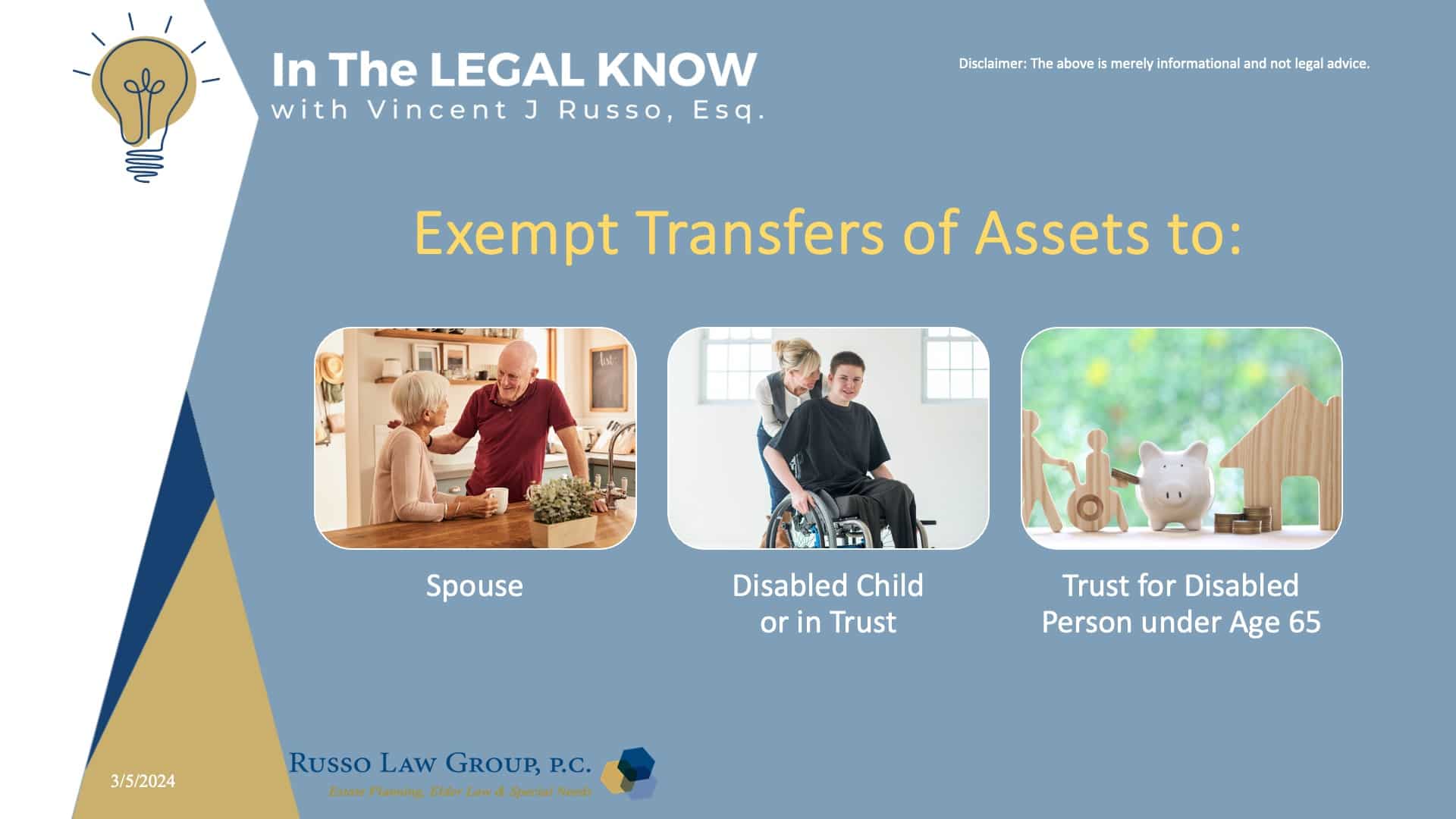

Let’s focus on the Exempt Transfer rules which allow you to make gifts in crisis to certain people without a penalty.

Under current law, certain transfers of assets by a Medicaid applicant or recipient do not result in any transfer penalties.

These exempt transfers of assets are:

- To the individual’s spouse or to another for the sole benefit of the individual’s spouse;

- From the individual’s spouse to another for the sole benefit of the individual’s spouse;

- To the individual’s child, or to a trust established solely for the benefit of the individual’s child. The child must be blind or permanently and totally disabled; or

- To a trust established for the sole benefit of an individual under 65 years of age who is disabled as defined under Supplemental Security Income (SSI) rules.

Although assets in any amount can be transferred to a disabled child of any age without affecting the Medicaid eligibility of the transferor, there are several other factors to consider.

The disabled child may be receiving government benefits, and it should be determined whether the transfer will affect the disabled child’s eligibility for such benefits. Additionally, the possible loss of a disabled child’s benefits will have to be weighed against the Medicaid benefit to the parent. That benefit would result from the transfer. If the disabled child is receiving SSI benefits, a transfer to the child could mean the loss of the child’s SSI. It could also mean the loss of Medicaid benefits as well.

Is there a different rule for transferring your home?

Yes, there is another set of rules for exempt transfers of the home:

A home is exempt if you reside there or intend to reside there, and it is in your own name subject to certain requirements. For example, in New York that amount is $1,071,000. Other states could be as low as $713,000. However, Medicaid will make a claim against your home when the Medicaid recipient passes away.

To avoid a Medicaid estate recovery, a home can be transferred without penalty to:

- the spouse of the individual;

- a child of the individual who is under age 21;

- a child who is blind or permanently and totally disabled;

- the sibling of the individual who has an equity interest in the home and who has been residing in the home for a period of at least one year immediately before the date the individual becomes institutionalized; or

- A son or daughter of the individual (other than a child as described above) who was residing in the home for at least two years immediately before the date the individual becomes institutionalized, and who provided care to the individual which permitted the individual to reside at home, rather than in an institution or facility.

What should I do if I am in crisis and in need of Nursing Home Care?

My advice is to immediately seek the counsel of an experienced elder law attorney. The attorney will need to assess your situation and consider the planning options that are available under the law. In many cases, some or all of the assets can be protected. However, the better course of action is to plan in advance.

Back on January 31st of this year, we discussed the use of a Medicaid Asset Protection Trust, and you can view that show on CFN Live or on In The Legal Know.

If you want more information, CLICK HERE to download our complimentary Medicaid Planning Guide.

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Related Posts

Comments (0)