This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/aQgwbQkJtC0 How can SSI…

Life Estates: Helpful or Problematic? (Part 2: Taxes)

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/_XxjAvWfrqs

Life estates are an estate planning tool when planning with residences. Before we get into taxes, let’s do a brief review of “What is a Life Estate?”

A life estate is an interest in real property where one has the exclusive right to use, occupy and possess the property for their lifetime. Typically, it is the owner of the residence that retains a life estate while transferring ownership to another person.

How are real estate taxes treated when there is a life estate?

First, the life tenant is responsible for the real estate taxes on the property. In fact, the life tenant must maintain and pay for the on-going costs on the property, including property taxes and upkeep.

The life tenant is responsible for maintaining the property and refraining from “engaging in waste”, which is an activity which would prevent the next person in line from putting the property to full use.

Since the life tenant remains the owner for purposes of real property taxes, he or she continues to qualify for the School Tax Relief Program – the STAR Exemption in New York, Veterans’ Benefits, and any other property tax reduction available to the “owner” of the property.

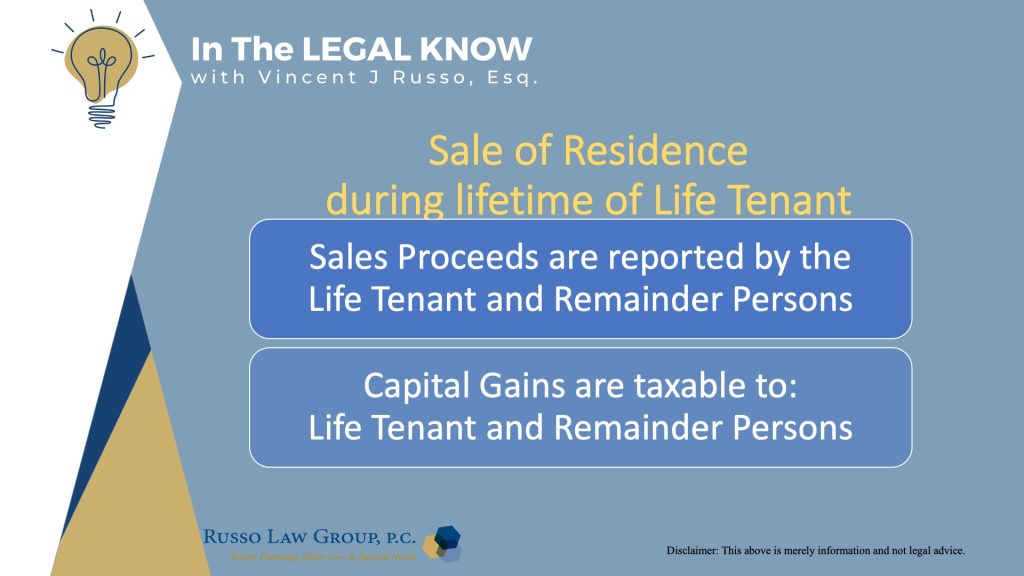

Who pays the capital gains tax if the house is sold during the life tenant’s lifetime?

Now, it gets more complicated. Since there is a split interest in ownership, both the life tenant and the remainder person will each receive a portion of the sale proceeds.

How this will be calculated depends on the purpose of the calculation. Under state real property law, there is a table to determine how much the life tenant shall receive based on their age.

For federal tax purposes, the sales proceeds are reported by the life tenant and remainder persons. There is another table that determines the life tenant’s share of the sale proceeds.

Capital gains are taxable in part to the life tenant and the remainder persons.

It is important to note that the life tenant will be eligible for a capital gain tax exclusion if they qualify. There is also a potential trap here because the remainder person will not be able to take advantage of the capital gains tax exclusion. This can be costly.

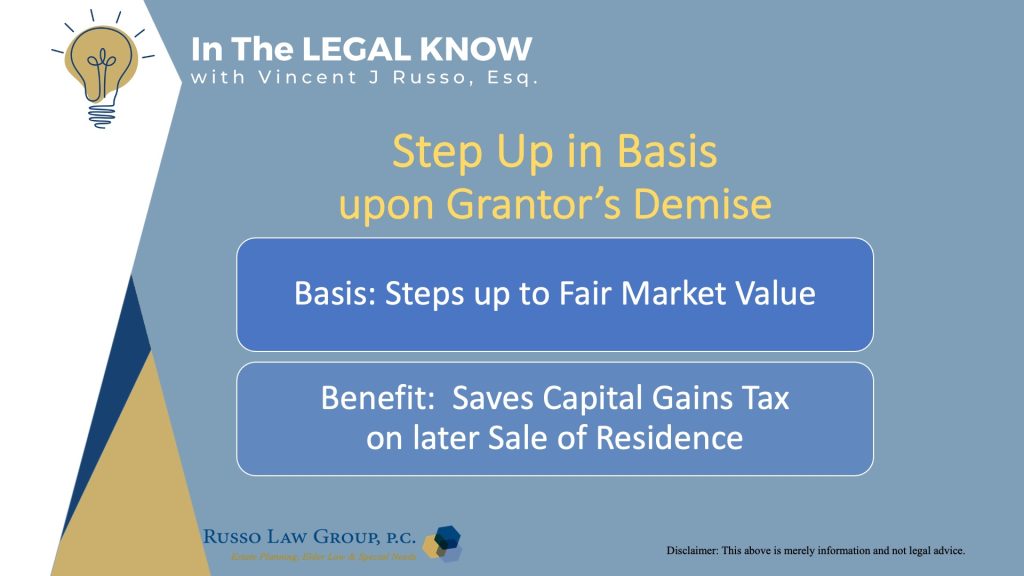

After the life tenant passes, are there any tax savings when the house is sold?

If the owner of the property is also the life tenant, then the property will be included in their taxable estate and the property will receive a step up in basis to fair market value upon the life tenant’s demise. This step-up in basis can save capital gains taxes on a later sale of the residence.

For example, let’s say mom transfers the home to her daughter while retaining a life estate. If her tax basis in the home is $250,000 and the home is worth $1,000,000 on her demise, the tax basis will step up to $1,000,000 and if sold at that time, there would be no capital gains tax. In my example, the step up could potentially save as much as $200,000 in taxes.

Also, before transferring the property, one should be aware that the initial transfer to the remainder person is subject to gift tax laws for the full amount. For most people, this is not an issue because of the $12,680,000 federal gift and estate tax exemption.

Tips for taxpayers who haven’t yet filed their income tax returns!

First, your tax returns must be filed by April 18th (postmarked and in the mail). If you need more time to file, you can file for an extension to October 16, 2023, to file your 2022 income tax returns.

Even though you file for an extension, you must pay any tax owed by tomorrow. You can pay the federal government online by going to: irs.gov/payments. This will avoid any penalties and interest if it is determined that you owe taxes when you file your return later.

If you are a New York resident, you must file for an extension separately and pay any estimated taxes owed by April 18th.

Want to learn more about life estates?

Click here to read PART 1 and click here to read PART 3: MEDICAID

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Related Posts

This Post Has 0 Comments