This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/mUrGKFJ5NOE The Silver Tsunami…

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/wZCIKdtScEo

When and how are gifts taxed?

At this time of year many people make gifts to family and charities. But many people are simply confused when it comes to gifts and the tax laws. To be clear, we are not talking about leaving an inheritance when one passes away. Instead, we are discussing lifetime gifts.

At this time of year many people make gifts to family and charities. But many people are simply confused when it comes to gifts and the tax laws. To be clear, we are not talking about leaving an inheritance when one passes away. Instead, we are discussing lifetime gifts.

Under federal law, a gift is when you give property (including money) without receiving something of at least equal value in return.

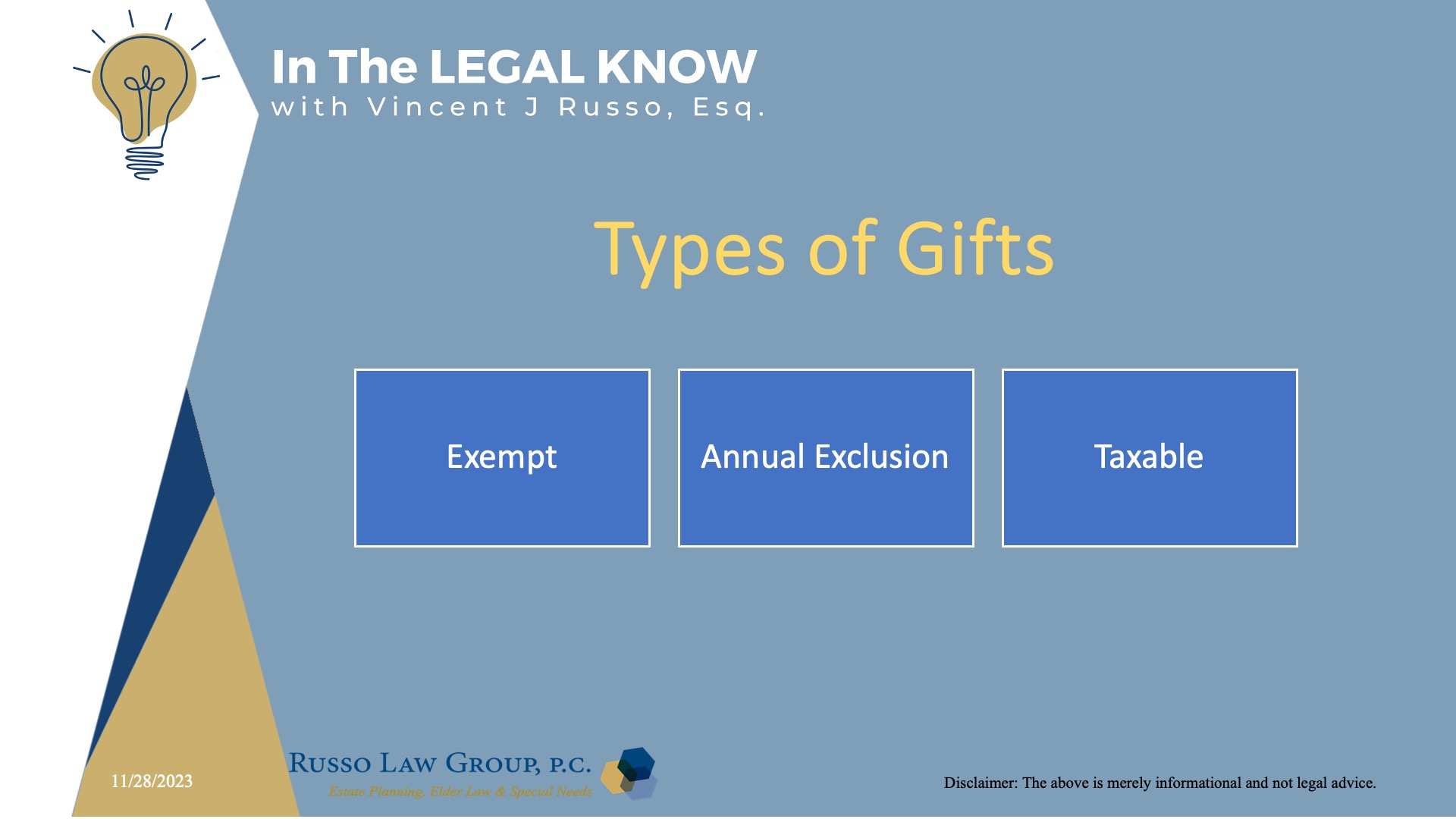

Gifts are subject to tax. But don’t be alarmed, there are: exempt gifts not subject to tax, annual exclusion gifts that are excluded from tax, and taxable gifts that are subject to tax but offset by a lifetime exemption. The gift tax rates go up to 40%.

Besides the federal gift tax law, Connecticut is the only state with a gift tax law as well.

We need to understand the following:

Which are the exempt gifts – not subject to tax?

An individual can make the following gifts without gift taxation:

These gifts can be made in addition to the annual exclusion gifts.

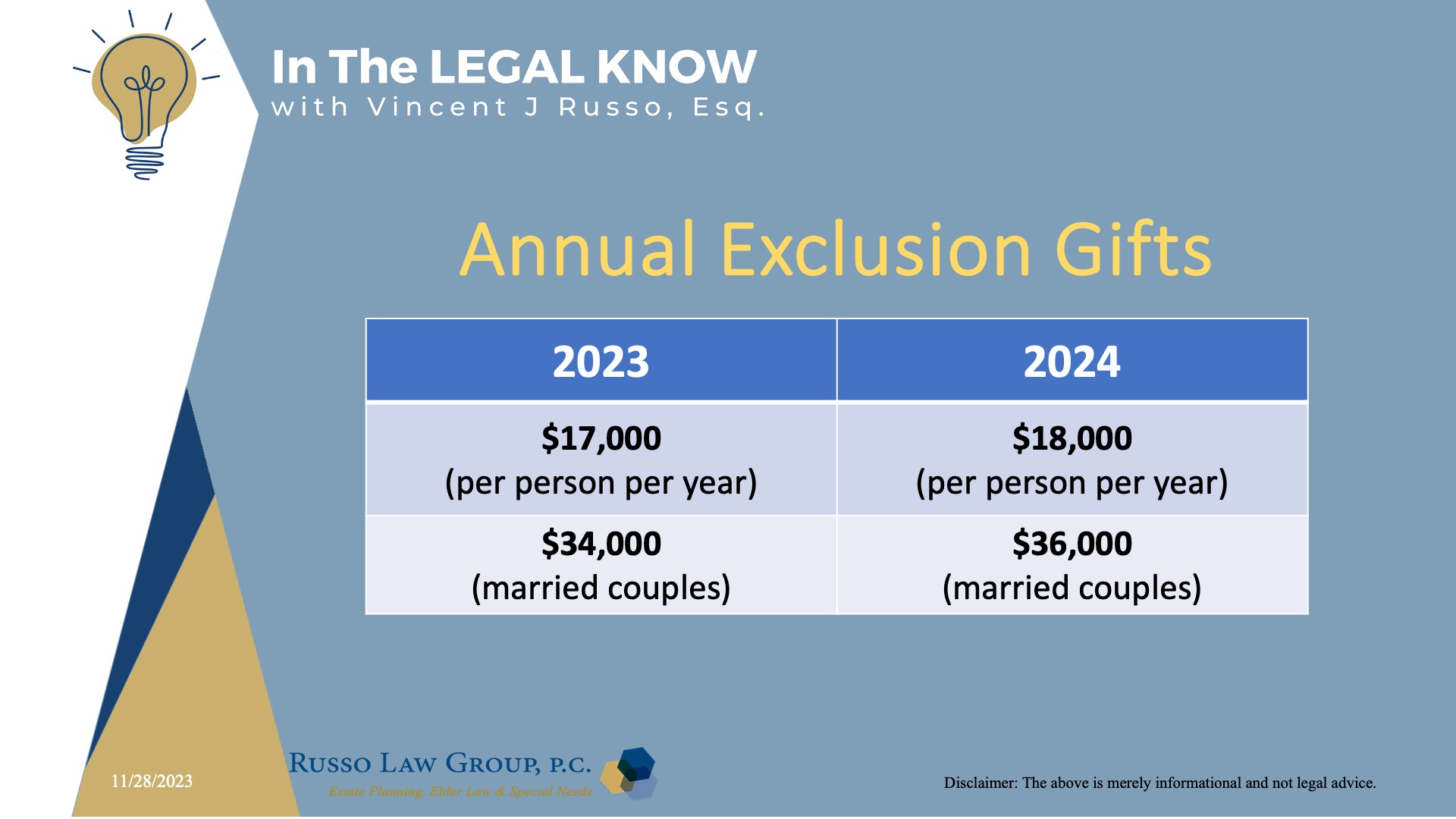

Are annual gifts subject to tax?

The short answer is no.

Annual exclusion gifts are gifts made up to $17,000 per person per year and those gifts are not taxed. That exclusion amount will go to $18,000 per person per year in 2024.

In addition, no gift tax return is required for these gifts.

If you are married, then you can double that amount, but you may have to file a gift tax return even though the gift is not subject to tax.

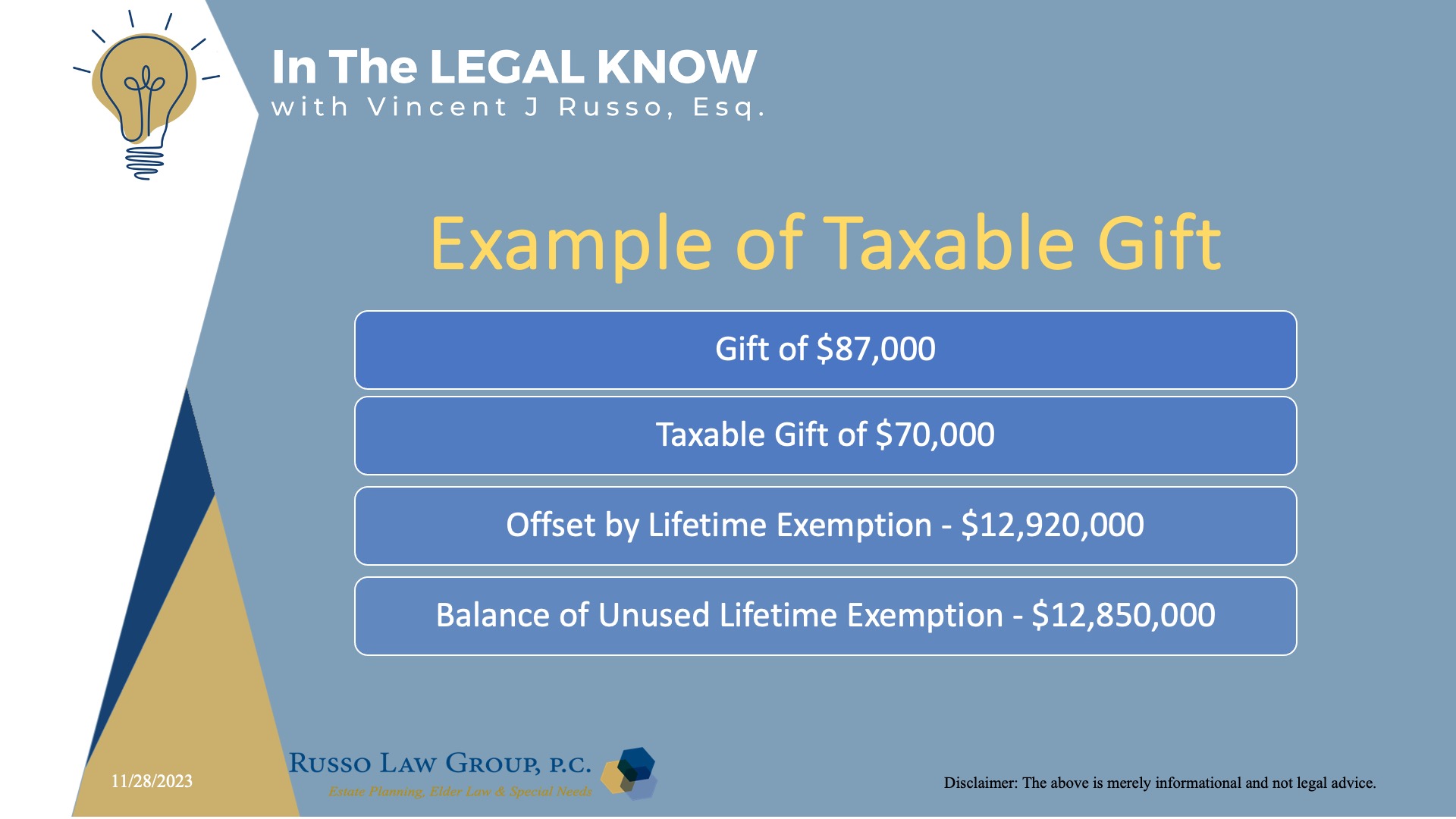

What happens if I make a gift over this amount?

If you make a gift over the annual gift exclusion amount (what I will call a taxable gift), you will have to file a gift tax return (Form 709) which is due by April 15th of the following year in which the gift is made.

The good news is that you will likely have no gift tax to pay because each US citizen is entitled to a lifetime gift and estate tax exemption which is currently $12, 920,000. That is a whole lot of gifting before a gift tax is owed.

If you make a gift of $87,000 to your daughter, the taxable gift would be $70,000 ($87,000 less $17,000). You would then file a gift tax return reporting the gift and you would use up $70,000 of your $12,920,000 exemption. No gift taxes would be owed, and you would still have an unused federal gift and estate tax exemption of $12,850,000.

One would only pay gift taxes if they exceeded their lifetime gift and estate tax exclusion amount. Since it is a unified gift and estate tax exemption, any unused gift exemption can be used to offset any estate taxes when one passes away.

Can I get a tax deduction for making a gift and does the recipient of the gift have to pay taxes?

First: a charitable donation to a qualified nonprofit may be tax deductible for income tax purposes.

Second: no – the person receiving the gift usually doesn’t have to report the gift or pay a tax on the amount received.

Gifts to spouses, charities and directly for tuition and medical expenses for another person are exempt. Gifts up to $17,000 per person per year are excluded. Gifts in excess of $17,000 are subject to tax offset by the lifetime gift exemption (currently $12,920,000).

The bottom line, no worries here (unless you are looking to make taxable gifts to save estate taxes and, in that situation, one should consult with a tax professional – advisor as to tax planning).

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Related Posts

Comments (0)