Discover the importance of the 10-Year Rule for inherited IRAs and what it means for your financial future.

What exactly is this 10-year rule regarding inherited IRAs?

The 10-year rule came out of the SECURE Act, which took effect in 2020. Additionally, it significantly altered how inherited IRAs are handled by most non-spouse beneficiaries.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/nm64M8_dVCE

This rule applies to most designated beneficiaries, which typically include adult children, grandchildren, siblings, other individuals who are not the surviving spouse of the IRA owner and certain trusts.

Under this rule, if you inherit an IRA from someone who was not your spouse, you are required to withdraw the entire balance of that inherited retirement account by December 31 of the tenth year following the year the original account owner passed away.

Under this rule, if you inherit an IRA from someone who was not your spouse, you are required to withdraw the entire balance of that inherited retirement account by December 31 of the tenth year following the year the original account owner passed away.

If the original owner passed away after starting their RMDs, the beneficiary must take annual required distributions in years 1-9, plus empty the account by year 10.

If the original owner passed away before starting their RMDs, the beneficiary must empty the account by year 10. There is no requirement to take specific minimum amounts in any given year from years 1 -9.

This is a major departure from previous rules, which allowed many beneficiaries—particularly children and grandchildren—to “stretch” required minimum distributions (RMDs) over the course of their own life expectancy. That approach let the account grow tax-deferred for decades and often reduced the annual tax burden.

Now, with the 10-year rule, the opportunity for long-term tax deferral is lost. Beneficiaries may face larger taxable withdrawals in a shorter timeframe, which could push them into higher tax brackets during those years. It’s a big shift that impacts both financial planning and tax strategies for families inheriting retirement accounts.

There is also a 5-year rule for estates, charities and some trusts.

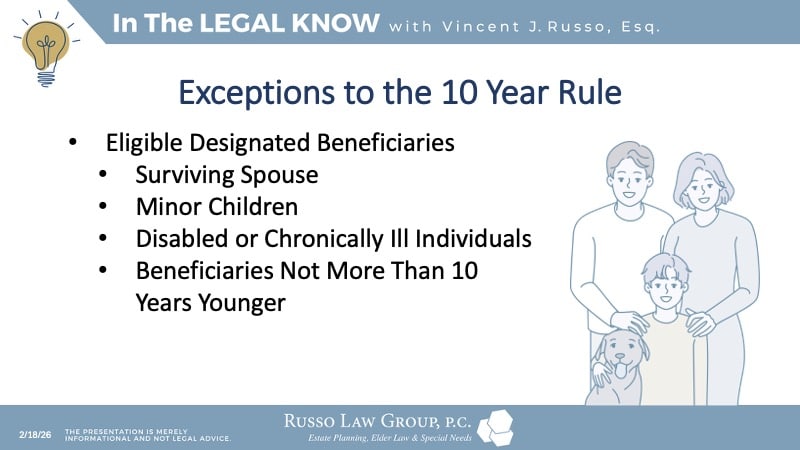

It’s important to note that this 10-year rule generally applies to anyone who is a Designated Beneficiary who does not fall into one of the exempted categories (referred to as “Eligible Designated Beneficiaries”).

What is the exception for Eligible Designated Beneficiaries?

There are some important exceptions. The rule does not apply to “Eligible Designated Beneficiaries,” and each category has its own unique considerations:

- Surviving Spouse: A spouse who inherits an IRA has the greatest flexibility. They can choose to treat the IRA as their own, roll it over into their personal IRA, or remain as a beneficiary. This allows for continued tax-deferred growth and the ability to use required minimum distributions (RMDs) based on their own life expectancy.

- Minor Children of the Original Account Owner: Minor children (but not grandchildren) can stretch distributions over their life expectancy until they reach the age of majority, as defined by their state—typically 18 or 21. Once they reach that age, the 10-year rule takes effect, requiring the remainder of the account to be withdrawn within the next 10 years.

- Disabled Individuals: Beneficiaries who are deemed disabled under IRS guidelines can also stretch distributions over their life expectancy. The definition of disability generally matches Social Security’s standards, meaning the individual must be unable to engage in substantial gainful activity due to a physical or mental impairment.

- Chronically Ill Individuals: This category refers to those with chronic illness, as certified by a physician. These beneficiaries can distribute inherited IRA assets over their life expectancy, preserving the tax advantages for a longer period.

- Beneficiaries Not More Than 10 Years Younger Than the Original Account Owner: This includes siblings, friends, or even other family members close in age to the deceased account owner. If the beneficiary is less than 10 years younger, they can use their own life expectancy for required distributions.

These individuals may still have the option to take distributions over their life expectancy, though the rules and definitions for each group must be carefully reviewed.

For example, a minor child will become subject to the 10-year rule once they reach age 21. It’s a nuanced area, so it’s always best to consult with a professional to fully understand which rules apply to a specific beneficiary.

What are some strategies to manage or defer taxes on inherited IRAs?

The planning has become more complex. One effective strategy is for the beneficiary to carefully time withdrawals over the 10-year window to minimize their overall tax burden.

- Over the 10-year period, beneficiaries can choose to take larger withdrawals (even if not required to) in years when their income is lower and smaller or no withdrawals in years when their income is higher.

- For example, if the beneficiary is planning to retire or expects a reduction in income within that 10-year period, they could delay larger withdrawals until their tax rate drops, reducing the overall tax hit.

- Another approach involves the original account owner considering a Roth IRA conversion before death. By paying the income taxes on the conversion during their lifetime—ideally in years when their personal tax bracket is lower—the owner allows beneficiaries to inherit a Roth IRA.

- Roth IRAs do not trigger taxable income upon withdrawal by the beneficiary, provided certain conditions are met, which can be a substantial advantage for heirs.

- Additionally, families may think about integrating charitable giving into their strategies. If a portion of an IRA is left to a qualified charity, that share passes income tax-free to the organization, while other assets can be left to individual beneficiaries.

- For some, using trusts—like see-through or accumulation trusts—may provide greater control over how and when distributions are made to heirs, although recent IRS rules have made trust planning more nuanced and require careful drafting to maintain favorable tax treatment.

- Finally, it’s always essential to work with both tax and legal advisors.

Each beneficiary’s situation is different, and a professional can help chart a withdrawal schedule or explore advanced tax strategies, such as bunching deductions in years of higher distributions, to further mitigate the tax impact of inheriting an IRA under the 10-year rule.

Tips for someone planning to leave their IRA to a loved one?

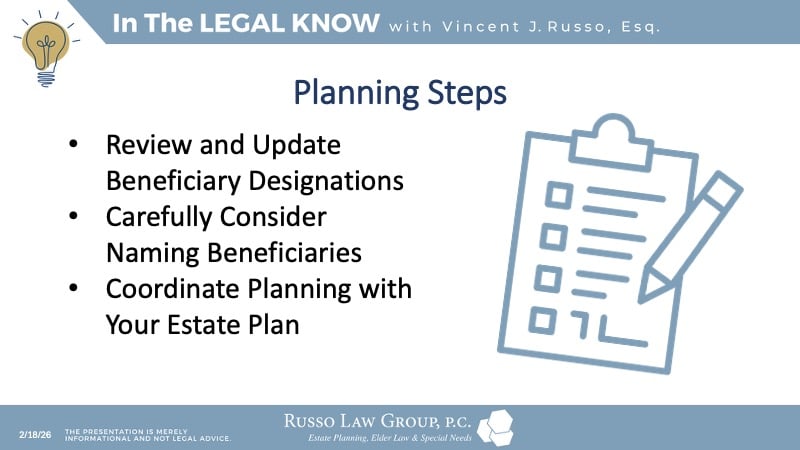

The most important thing is to be proactive and intentional with your planning.

- Start by reviewing and updating your beneficiary designations on all IRA accounts on a regular basis, especially after major life events such as marriage, divorce, birth of a child, or the death of a loved one. Remember, the beneficiary form on file with your IRA custodian overrides what’s written in your will or trust, so ensure it aligns with your current wishes.

- Next, carefully consider who you are naming as beneficiary. If you have concerns about a beneficiary’s ability to manage a substantial inheritance, or if you want to protect the assets from creditors or divorcing spouses, it is worth exploring the use of a trust as the IRA beneficiary.

- This allows you to tailor the timing and conditions of distributions according to your preferences, such as staggering payments over time or providing for a minor or special needs beneficiary.

- However, the trust must be properly drafted to comply with both IRS rules and your estate goals. Specific language and structure are required to ensure the trust qualifies for favorable tax treatment and that stretch options, if available, are preserved for eligible designated beneficiaries.

- Additionally, it’s important to coordinate your IRA planning with the rest of your estate plan. Work closely with both an estate planning attorney and a financial advisor to evaluate how inherited IRAs will affect your overall wealth transfer strategy and potential tax liabilities for your heirs.

- Consider Roth conversions if appropriate for your situation, and discuss the impact of changing laws on retirement account distributions. Regularly communicate your intentions to family members or potential beneficiaries so they are prepared for their roles and responsibilities.

In summary, thoughtful planning, up-to-date beneficiary forms, consideration of trusts, coordination with your total estate plan, and consultation with professionals are all key steps to ensure your IRA is passed on according to your wishes, while minimizing complications and maximizing potential benefits for your loved ones.

Advice for someone who has just received an inherited IRA?

First and foremost, resist the urge to make immediate decisions or withdrawals from the inherited IRA, as acting too quickly without understanding the rules can lead to costly mistakes.

Begin by determining exactly which type of beneficiary you are. Whether you are:

- an Eligible Designated Beneficiary (such as a spouse, a minor child of the original owner)

- a disabled or chronically ill individual

- someone not more than ten years younger than the account holder

- or a standard designated beneficiary.

Your beneficiary status will dictate what distribution options and timelines are available to you under the 10-year rule.

Next, ensure the inherited IRA is retitled correctly, reflecting both the original owner’s name and your status as the beneficiary (for example, “John Smith, deceased, IRA FBO [Your Name], beneficiary”).

Improper titling can unintentionally accelerate required distributions or even cause the account to be treated as fully distributed, resulting in immediate taxation on the entire balance. Never commingle an inherited IRA with your own retirement accounts! It must remain distinct to preserve its inherited status and the corresponding distribution timeline.

Before taking any distributions, review your income situation and consider the tax implications of withdrawals over the 10-year period. It may be best to coordinate distributions with expected changes in your income or tax bracket such as anticipated retirement, career changes, or years with large deductible expenses—to optimize tax efficiency. For inherited Roth IRAs, it’s important to review whether the 5-year holding period was met to ensure distributions are tax-free.

If you would like to speak with an experienced elder law attorney regarding your situation or have questions about something you have read, please do not hesitate to contact our office at 1 (800) 680-1717. We look forward to the opportunity to work with you.

Disclaimer: The information provided above is for general informational purposes only and is not legal advice.

Related Posts

Comments (0)