Understand the intricacies of tax return filings. Vincent J. Russo shares crucial insights to make filing easier.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/jzGyAUvH02M

What is a Reverse Mortgage?

A reverse mortgage loan is like a traditional mortgage. Homeowners borrow money from a lender using their home as security for the loan. Also like a traditional mortgage, when you take out a reverse mortgage loan, the title to your home remains in your name.

However, unlike a traditional mortgage, with a reverse mortgage loan, borrowers don’t make monthly mortgage payments. The loan is repaid when the borrower no longer lives in the home. Interest and fees are added to the loan balance each month and the balance owed grows.

You can get a Home Equity Conversion Mortgage (HECM) loan of up to $1,089,300 in 2023.

What are the benefits of a reverse mortgage?

A reverse mortgage can be very helpful. Here are some of the primary benefits:

- It allows you to stay in your home. The funds from the reverse mortgage can pay for your housing costs (taxes, insurance, repairs). For example, making home improvements to age in place with a reverse mortgage may be more affordable than selling and downsizing your home.

- You’ll have more financial freedom. If you choose to receive payouts from your reverse mortgage on a monthly basis, you’ll have a reliable flow of cash in your budget to help cover your living expenses.

You can also use reverse loan funds however you’d like, giving you the flexibility to do what’s important to you and your family. For example, you can help a child out with college tuition. Additionally, you could renovate your home to meet special needs as you or a loved one ages.

- You can pay off debt.If you have unpaid medical bills or high-interest debt, you can pay off your balances with the funds from a reverse mortgage.

- Your spouse can stay in the home after you die or move out.Even if your spouse wasn’t a co-borrower on the loan, they can stay in the home after you die or move into a long-term care facility — provided you were married at the time you took out the reverse mortgage. However, they must meet certain conditions set by the U.S. Department of Housing and Urban Development (HUD).

There are some additional benefits, such as

- Your reverse income is not taxed.The IRS doesn’t consider reverse mortgage payments as income, so they aren’t taxable — regardless of whether you receive them as a lump sum, monthly income, line of credit or any combination of the three, and

- You won’t leave an underwater home to your heirs. Reverse loans have built-in protections that limit your heirs’ responsibility for any remaining balance after you die.

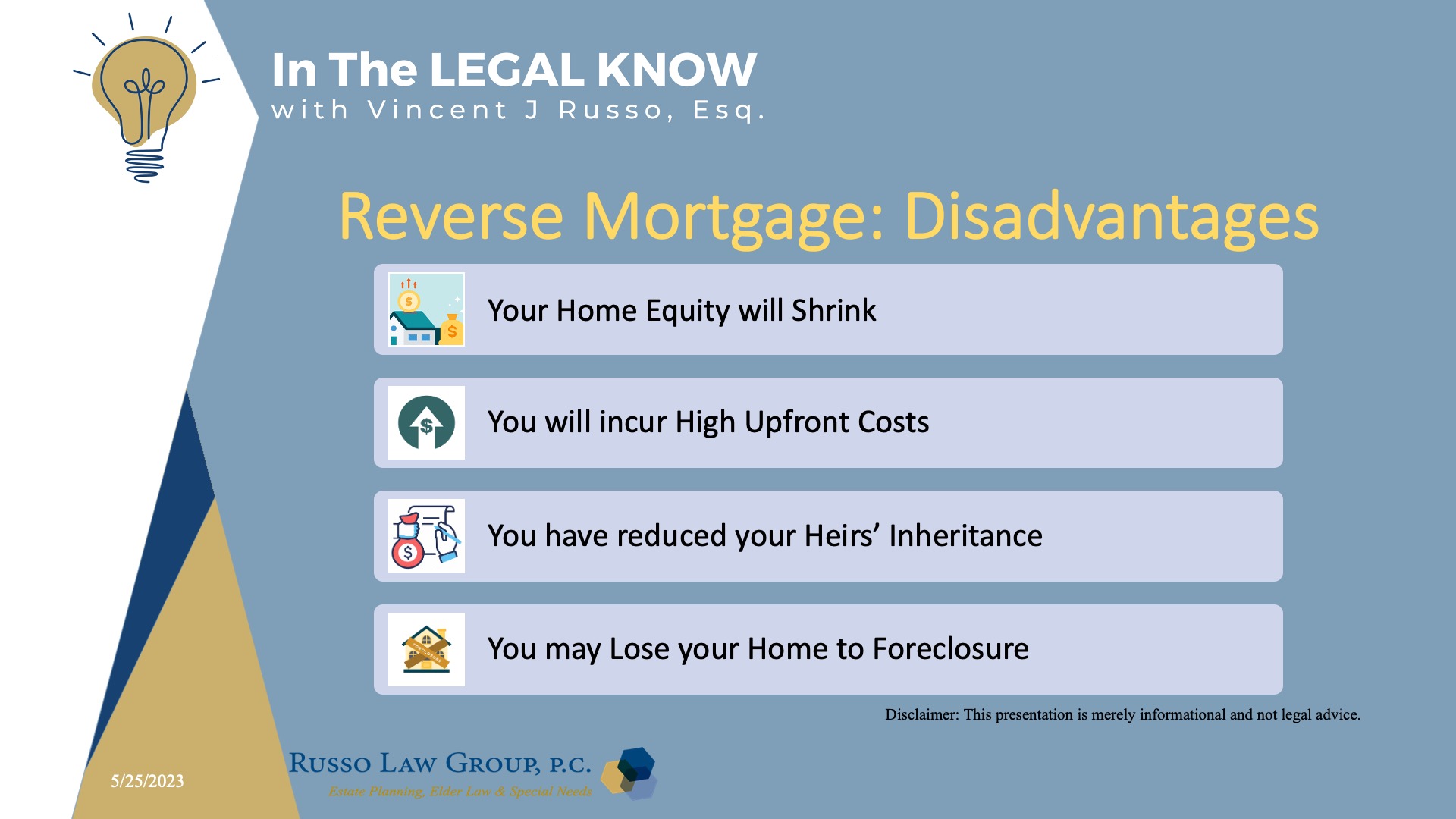

What are the disadvantages?

There can be a number of disadvantages:

- Your home’s equity will shrink. A big downside to reverse mortgages is the loss of home equity. Because you’re not paying down your reverse mortgage balance, you’ll make less profit when you sell, or limit your borrowing power if you need a new loan.

- You’ll pay high upfront fees.With loan origination fees up to $6,000, upfront mortgage insurance premiums worth 2% of your home’s value and other closing costs. Reverse mortgages are more expensive than other home loan types. You’ll also pay origination fees at closing. You do have the option of rolling these costs into your loan balance, but that means you receive less money.

- You’ll reduce your heirs’ inheritance.As a reverse mortgage balance grows, the equity your heirs would receive is diminished. If they can’t repay the loan when you pass away or move, they won’t be able to keep the home.

- You might lose your home to foreclosure.You’re still responsible for paying property taxes and insurance, and if you default on your property taxes, you could lose your home to tax foreclosure. A reverse mortgage lender can foreclose on the home if you’re not living in it for more than 12 consecutive months due to health care issues.

Also, upon borrower’s passing, the balance of the loan becomes due. Your heirs must determine whether they would like to keep the property. If they wish to keep it, they must satisfy the loan in its entirety. Otherwise, they can sell the property if they do not wish to or cannot afford to keep the home. If they fail to take any action, the loan will be foreclosed upon. As a result, the lender will force the sale of the home.

How do reverse mortgages work under the Medicaid rules?

Under the Medicaid rules, Reverse Mortgage Payments are exempt, provided the payments are spent during the month received; any amount not spent will be a countable resource the following month.

To benefit from a reverse mortgage without losing Medicaid or SSI coverage, one should obtain a reverse mortgage through a line of credit. With a line of credit, the senior could withdraw and spend funds in a calendar month, as needed. This can be done without adversely affecting their Medicaid and SSI coverage.

If you are on Medicaid or are considering going on Medicaid, I highly recommend that you seek the services of an elder law attorney so that you understand what you need to do from a Medicaid eligibility standpoint.

Who is best suited for a reverse mortgage and who is not?

Here are a few rules of thumb that can help you evaluate whether a reverse mortgage makes sense in your situation.

Assuming you meet the qualification rules, a reverse mortgage may be a good idea if:

- You and your spouse want to and are able to stay in your home.

- You need additional funds to cover living expenses, pay for care or enhance your lifestyle.

- You’ve considered the needs of your heirs.

- You’ve built enough equity that after paying off any existing mortgage debt, you have sufficient funds to cover your on-going needs.

- Your home value is or has been increasing.

A reverse mortgage is likely a bad idea if:

- You feel strongly that your home should stay in the family when you die.

- You became disabled or need long term care that would lead you to move in with a family member in their home, or a long-term care facility.

- Your health is shaky or unpredictable.

- You’re planning to move soon.

Once again, it is important to get professional advice before signing up for a reverse mortgage. Additionally, as I mentioned, one of the requirements of getting a reverse mortgage is that you have go to a HUD counselor first which will prove to be helpful as well.

Click here to download our free informational pamphlet on Reverse Mortgages

Want to learn more about reverse mortgages?

Click here to read PART 1

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Related Posts

thanks

Thank you