In the big picture, since the tax world is constantly changing, this tax season is no different, with a myriad of rules, deductions, credits, and responsibilities that may seem overwhelming.

A Pooled Income Trust in New York can mean the difference between being able to stay at home or being forced into a nursing home for long term care.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/khXgK54NNRQ

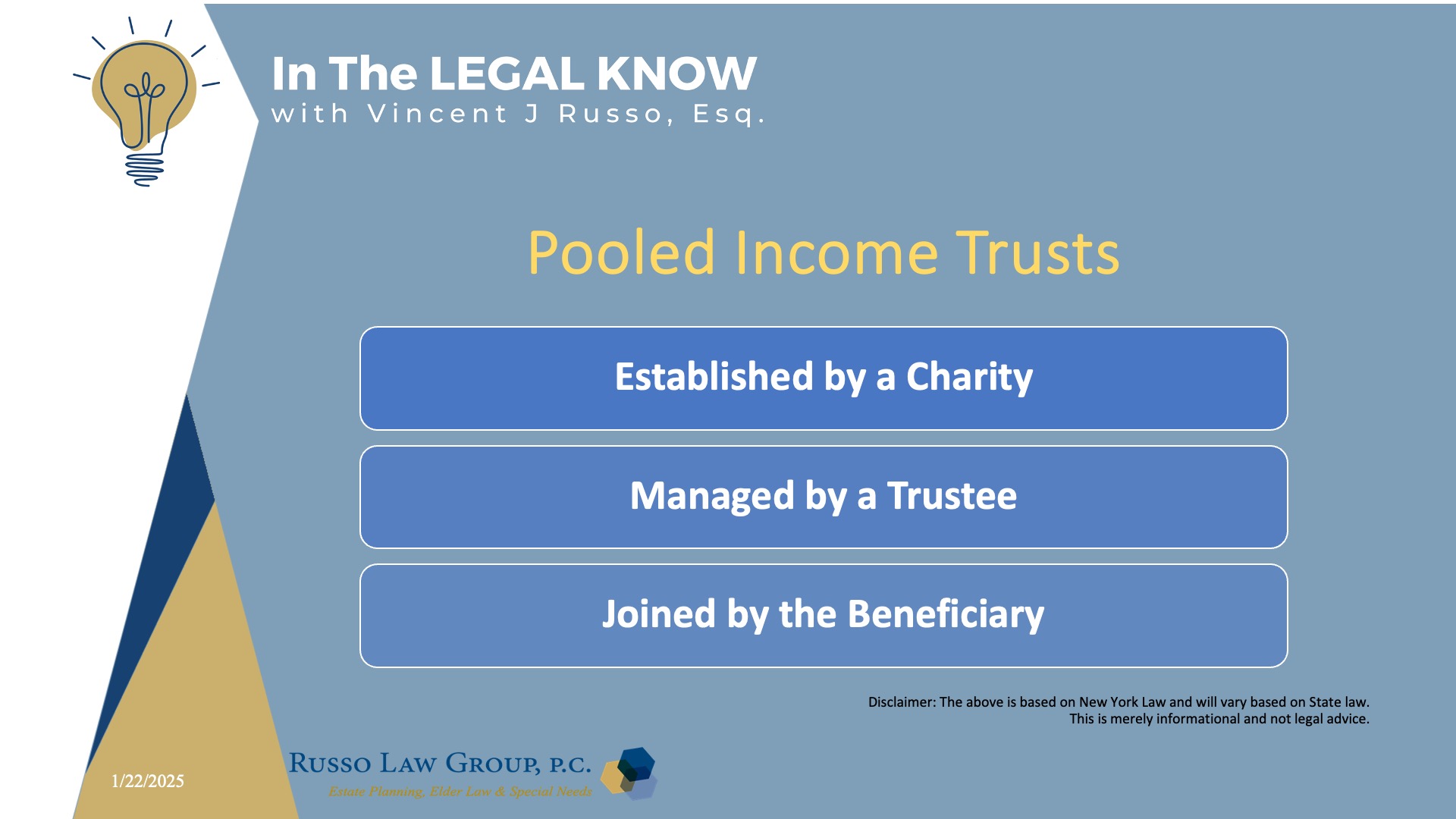

What is a Pooled Trust

A “pooled supplemental needs trust” is a type of special needs trust where multiple individuals with disabilities contribute funds to a single, collectively managed trust, allowing them to access government benefits like Medicaid while still utilizing their excess assets to pay for additional needs not covered by those benefits; essentially, it enables people to “spend down” their assets to qualify for Medicaid while still having access to funds for supplemental care through the pooled trust.

A “pooled supplemental needs trust” is a type of special needs trust where multiple individuals with disabilities contribute funds to a single, collectively managed trust, allowing them to access government benefits like Medicaid while still utilizing their excess assets to pay for additional needs not covered by those benefits; essentially, it enables people to “spend down” their assets to qualify for Medicaid while still having access to funds for supplemental care through the pooled trust.

Pooled Trusts give people with disabilities a way to access vital health benefits while utilizing the excess funds they deposit into the trust to pay for items and services not covered by those benefits.

How can seniors in New York benefit by setting up a Pooled Income Trust?

In New York, there is a particular type of Pooled Trust called a “Pooled Income Trust” which allows seniors and people with disabilities to protect your monthly income while accessing Medicaid home care services.

Seniors are allowed to keep a certain amount of monthly income. In 2024, that amount was $1,752. Any monthly income above that amount, referred to as “Excess Income” must be spent down on home care services before Medicaid pays for these services.

And that is the dilemma. How does one afford to stay at home if they can’t use their excess income to pay for living expenses and this is where the Pooled Income Trust comes to the rescue.

Who is eligible for a Pooled Income Trust and what are the advantages?

New York residents of any age who are disabled as defined by Social Security Law can establish a pooled trust to deposit excess monthly income and/or resources so that those funds are no longer considered when determining a person’s eligibility to receive services through means-tested government benefits.

For many seniors who want to stay at home but need long term care, the Medicaid home care program will not help because they have too much monthly income. Seniors are forced to spend down monthly income before they can receive Medicaid home care services in New York. This loss of income can have a dramatic impact on that person’s ability to remain in the community and their quality of life.

Who can create a Pooled Income Trust?

There are strict rules on who can set up a Pooled Income Trust.

A Pooled Income Trust can only be established by a Charity and is managed by a Trustee. The Senior (or his/her legal representative) can then establish a segregated account with the Pooled Trust by signing a joinder agreement and funding the account with the senior’s excess monthly income.

Then, the funds in the account can be used for the benefit of the senior, such as paying for rent, real estate taxes, living expenses, and repairs to the home.

Any remaining funds in the beneficiary’s account upon their demise are utilized to support other people with disabilities. Otherwise, these funds must be paid over to New York State to reimburse them for the Medicaid coverage that was provided.

One of the benefits is that the senior gets professional trustee to manage their account. Typically, there is a one-time set-up fee (ranging from $150 – $200) and a monthly fee (ranging from $30 to $175 per month) depending upon the Pooled Income Trust selected (often based on the amount of monthly income).

What is “Excess Monthly Income” and are there consequences?

Excess monthly income is the amount of money you must spend on home care before Medicaid will cover you.

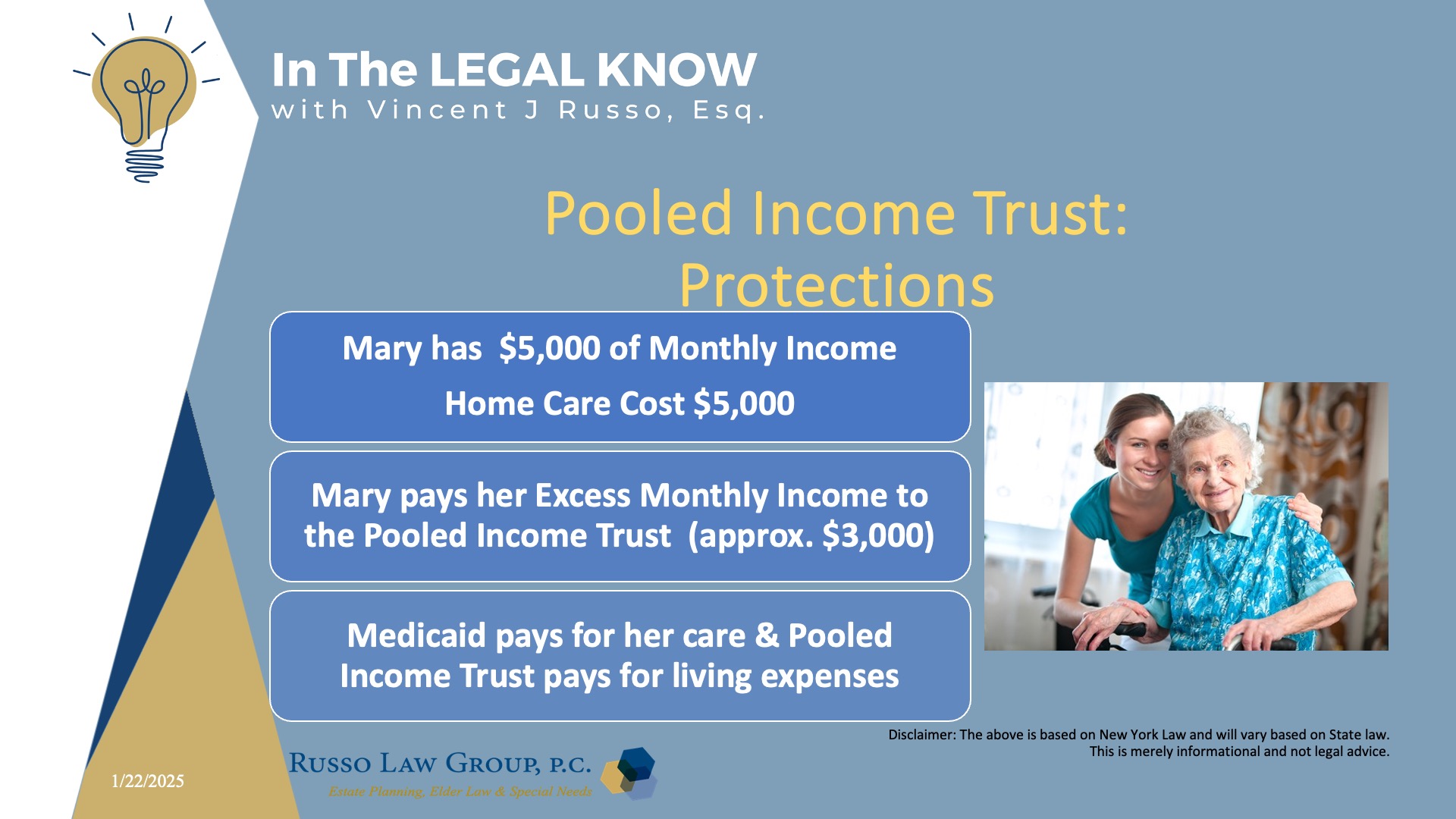

For example, Mary needs long-term care, and she wants to stay in her home. Mary needs Medicaid to pay for her long-term care, which would cost $5,000 per month but she only has $5,000 of monthly income.

In New York, Medicaid says that she would have to spend down each month her excess income ($3,248 in 2024) but she needs that money to live on – to pay for food, clothing, and shelter.

Now, instead of being forced to spend that excess income on her care each month, she can pay those funds to her Pooled Income Trust account and then the funds can be used to pay for living expenses and supplement her Medicaid home care. Mary can stay at home where she wants to be.

Without that protection, Mary would not be able to keep her home.

There are over 20 Pooled Income Trusts to choose from in New York and an experienced elder law can help you select the appropriate Pooled Income Trust for you.

What are the top advantages of a Pooled Income Trust?

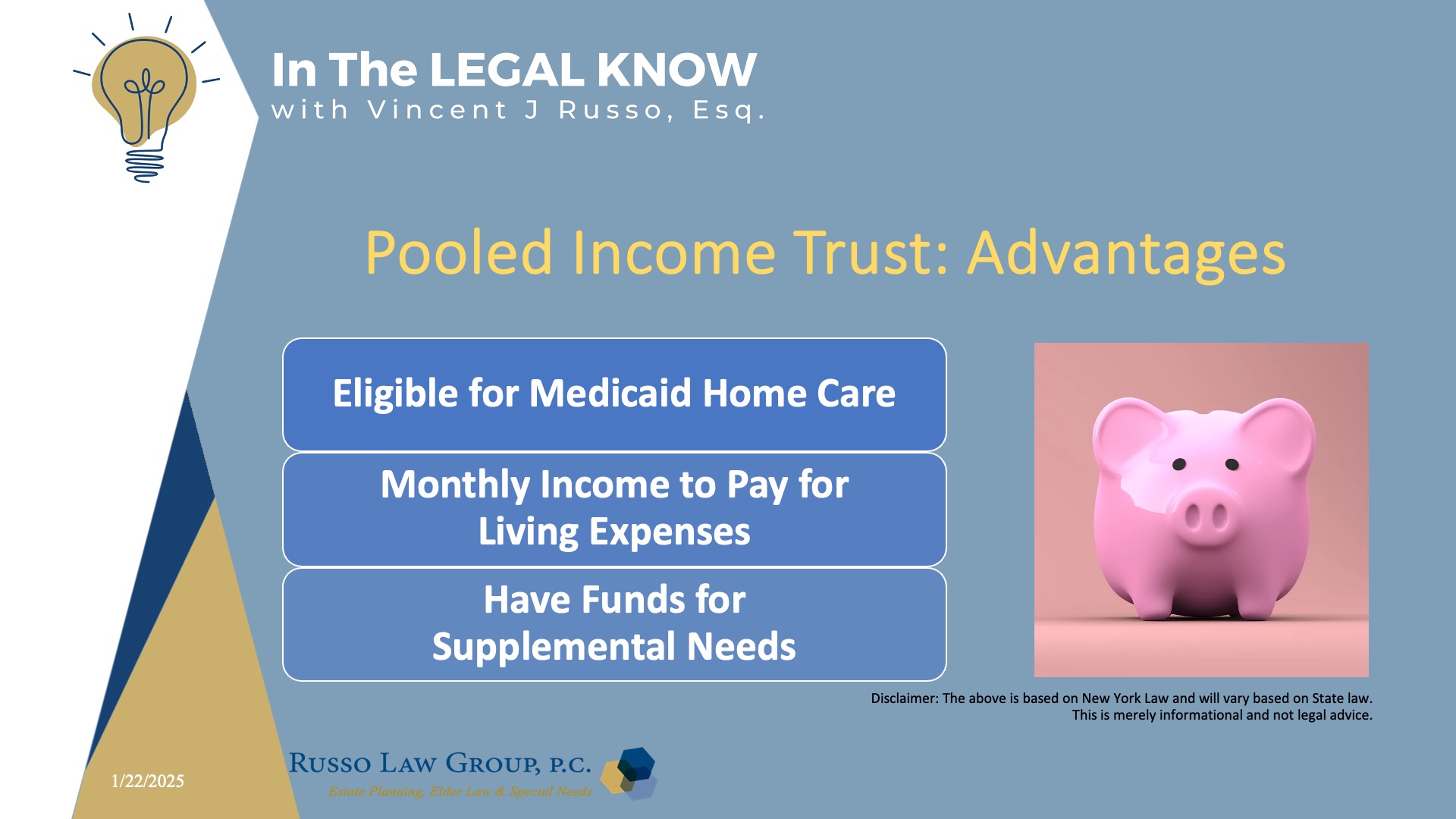

Let’s summarize the advantages:

NYS Pooled Income Trusts allows seniors to:

- Qualify and Maintain Eligibility for Medicaid Home Care Benefits

- Protect Monthly Income to pay for Living Expenses

- Protect Funds for Supplemental Needs that enhance one’s quality of life

There is also the additional benefit of low set up costs and monthly fees charged by the Trustee (in comparison to fees involved with a First Party Special Needs Trust).

Theresa Foundation Pooled Trusts

The Theresa Foundation supports programs for children with special needs in the areas of music, dance, art, and recreation. As an effort to help seniors and younger people with disabilities, the Theresa Foundation has created the Theresa Pooled Income Trust in New York.

At theresapooledtrust.org, you will find all the information you need to open a Theresa Pooled Income Trust account. For seniors, this step will protect your monthly income while allowing you to access Medicaid home care.

In the alternative, you can call at 516-432-0200.

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Disclaimer: The information provided above is for general informational purposes only and is not legal advice.

Related Posts

Comments (0)