Understand inherited IRAs and the 10-year rule under the SECURE Act. Learn how to manage your inherited retirement accounts.

Navigating the complexities of Medicare can be daunting, and Older Adults are confronted with making decisions regarding their health care coverage during the current Medicare Open Enrollment period.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/AOET_-uKMyE

What does it mean for Medicare beneficiaries that they are in the Medicare Open Enrollment?

Every year there are changes to Medicare, Medicare Advantage Plans and Medicare Prescription Drug Plans (PDPs). 2026 is no exception. We are now in the annual Medicare open enrollment period for Medicare which runs from October 15th to December 7th.

Every year there are changes to Medicare, Medicare Advantage Plans and Medicare Prescription Drug Plans (PDPs). 2026 is no exception. We are now in the annual Medicare open enrollment period for Medicare which runs from October 15th to December 7th.

During this time, people with Medicare can review features of Medicare plans offered in their area and make changes to their Medicare coverage, which go into effect on January 1st of 2026.

These changes include switching from traditional Medicare to a Medicare Advantage plan (or vice versa), switching between Medicare Advantage plans, and electing or switching between Medicare Part D prescription drug plans.

Medicare Open Enrollment is essential because your healthcare needs change over time. What worked last year might not be the best option this year. By reassessing your plan, you can potentially save money, gain better coverage, or find a plan that includes your preferred healthcare providers. With rising healthcare costs, taking advantage of this period can lead to significant financial and health benefits.

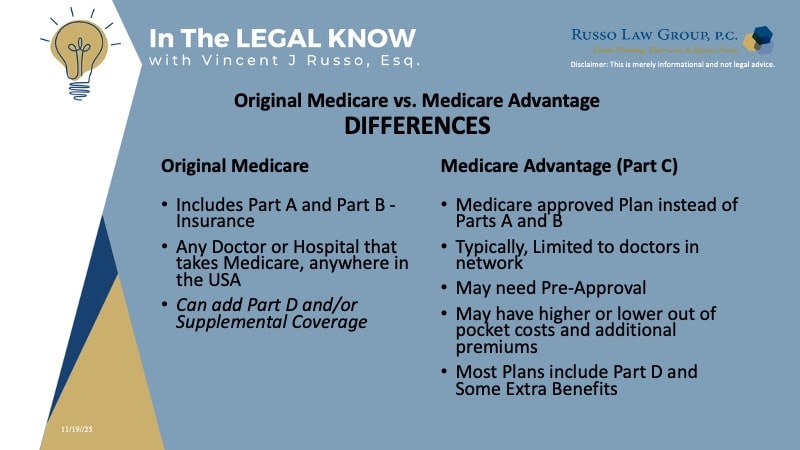

What are the differences between Original Medicare and Medicare Advantage?

Original Medicare includes Part A (hospital insurance) and Part B (medical insurance). You can add Part D for prescription drugs, and many people also buy supplemental “Medigap” coverage to help pay out-of-pocket costs. With Original Medicare, you can see any doctor or hospital in the U.S. that accepts Medicare.

Medicare Advantage (Part C) is offered by private insurance companies and bundles Parts A and B, and usually Part D, into one plan. These plans often include extra benefits not covered by Original Medicare—such as vision, hearing, and dental. Some plans may also offer lower out-of-pocket costs, but you generally must use doctors and providers within the plan’s network.

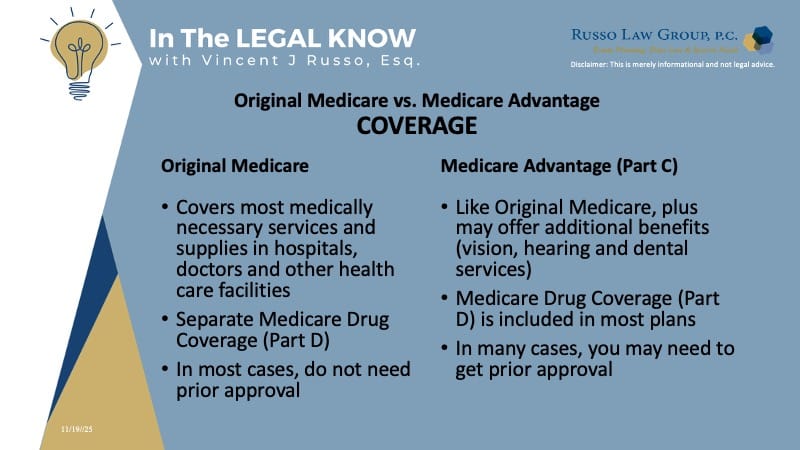

What are the differences in coverage?

Original Medicare covers medically necessary services and supplies from any provider that accepts Medicare, but it does not include certain routine benefits like vision, dental, and hearing. Prescription coverage requires enrolling in a separate Part D plan. You typically don’t need prior approval for services.

Medicare Advantage plans must cover everything Original Medicare covers, but many add extra benefits such as dental, hearing, and vision. Most plans include prescription drug coverage (Part D) and do not allow you to join a separate drug plan. However, many services may require prior authorization from the plan before they’re covered.

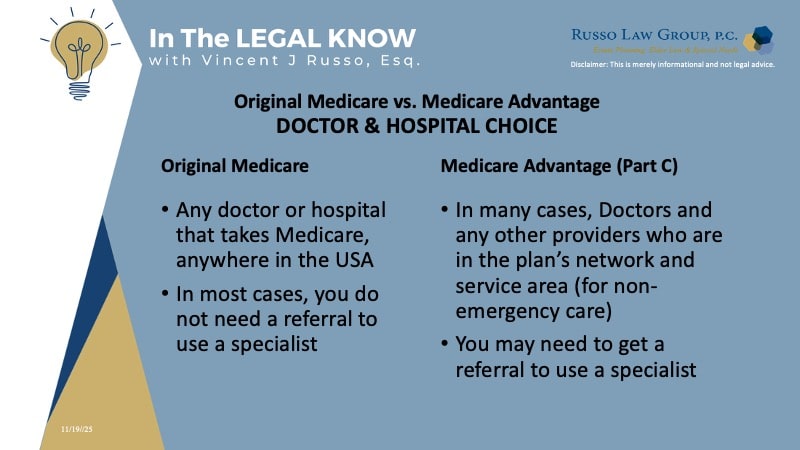

As to doctors and hospital choice, with Original Medicare, you can visit any doctor or hospital nationwide that accepts Medicare, without needing referrals for most specialists.

With Medicare Advantage, your options may be more limited. Most plans require you to use doctors and facilities within their network and service area. You may also need referrals to see specialists, and going out of network (when allowed) often comes with higher costs.

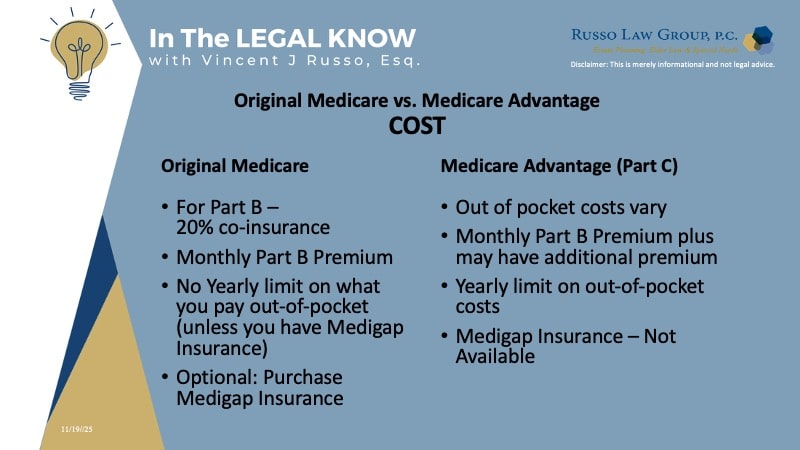

How much does Medicare Advantage cost compared to Original Medicare?

With Original Medicare, you pay 20% coinsurance for Part B services after meeting your deductible, along with a monthly Part B premium and possibly a separate premium for drug coverage (Part D). There’s no yearly limit on out-of-pocket costs unless you have supplemental coverage like Medigap, which you can purchase.

In contrast, Medicare Advantage plans may have varying out-of-pocket costs, often include drug coverage, and set a yearly limit on what you pay for services. You’ll still pay the Part B premium, and some plans may have an additional premium or even a $0 premium. However, Medigap isn’t available with Medicare Advantage.

How can one protect themselves against scammers during enrollment periods?

Scammers are extra busy this time of year. They may pretend to be from Medicare or an insurance company to try to steal your personal information — or even enroll you in a plan without your knowledge.

Remember, legitimate agents and brokers who represent Medicare plans need your permission before contacting you. If you get an unsolicited call, just hang up. Uninvited emails or texts? You can ignore those, too.

If you suspect Medicare fraud, report it immediately to Medicare at 1-800-MEDICARE or visit Medicare.gov/fraud.

And as always, never give your Medicare Number, Social Security number, or financial information to anyone you don’t know.

Navigating Medicare Open Enrollment can be complex, and making the wrong choices could leave you without essential coverage for unexpected challenges.

Medicare.gov/plan-compare is your official source to find the type of coverage that fits you best during Medicare Open Enrollment.

Older Adults should seek the assistance of professionals who can advise you on the best plan for you.

If you would like to speak with an experienced elder law attorney regarding your situation or have questions about something you have read, please do not hesitate to contact our office at 1 (800) 680-1717. We look forward to the opportunity to work with you.

Disclaimer: The information provided above is for general informational purposes only and is not legal advice.

Related Posts

Comments (0)