Whether you recently received one or are planning for the future, understanding how to keep…

Saving money is crucial for financial security, providing a safety net for emergencies, enabling long-term goals, and fostering financial stability. But what about taxes when you sell those assets and how can you avoid them?

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/FsV_x7Ca9t8

What is a “capital gain” and how it is taxed?

Let’s start at the beginning – there are two types of income that the federal government taxes: ordinary income or capital gains income. Ordinary income includes salary, interest income, self-employment income and rental income.

On the other hand, capital gains income results from the selling of certain personal items for more than you paid for them. Examples of transactions that can trigger capital gains tax include:

- Stocks sales

- Mutual fund sales

- Home sales

Capital Gains vs. Losses

To determine the extent of a capital gain or loss, you simply subtract your cost of the asset you sold from its sales price. If your cost is less than the sales price, you have a capital gain. If your cost exceeds your sales price, you have a capital loss.

To determine the extent of a capital gain or loss, you simply subtract your cost of the asset you sold from its sales price. If your cost is less than the sales price, you have a capital gain. If your cost exceeds your sales price, you have a capital loss.

You can deduct up to $3,000 in capital losses from your income each year. If your capital losses are more than $3,000, you can carry them forward to the next tax year.

Is there a difference in tax rates for ordinary income versus capital gains income?

Yes, there can be a large difference in the tax rates. In general, top ordinary income tax rates exceed top capital gains tax rates. Consequently, you prefer income to be from a capital gains transaction over an event triggering ordinary income.

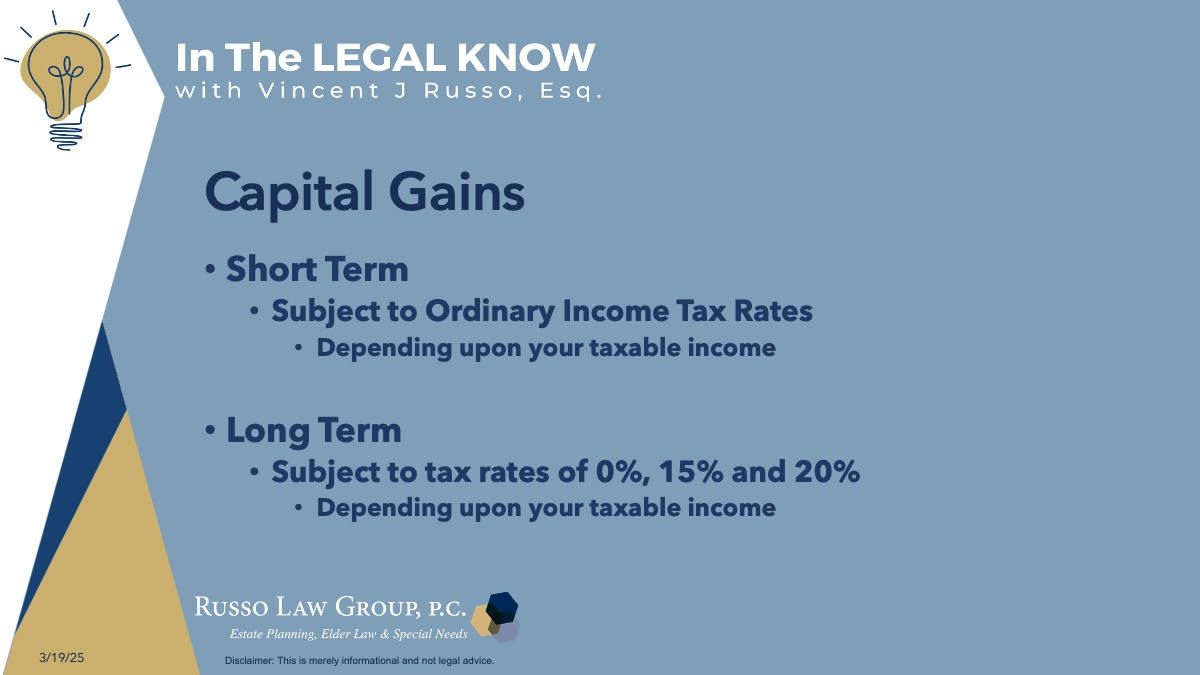

Short term capital gains – assets sold within one year of being purchased are subject to ordinary income tax rates. Long term capital gains are tax at preferential rates.

For 2025, the long-term capital gains tax rates range from 0 % to 20%. They are as follows:

- 0% Rate: For single filers with taxable income up to $47,025, and for married couples filing jointly with taxable income up to $94,050.

- 15% Rate: For single filers with taxable income between $47,026 and $518,900, and for married couples filing jointly with taxable income between $94,051 and $583,750.

- 20% Rate: For single filers with taxable income exceeding $518,900, and for married couples filing jointly with taxable income exceeding $583,750.

According to the IRS, the tax rate on most long-term capital gains is no higher than 15% for most people. And for some, it’s 0%.

For the highest earners in the 37% income tax bracket, holding investments for over one year could potentially reduce their capital gains tax rate to 20%. Keep in mind that some high earners may be subject to an additional 3.8% net investment income tax regardless of when they sell for a profit.

Are there strategies on how to avoid the capital gains tax?

Let’s start with two basic strategies to avoid or minimize capital gains tax.

Strategy #1: Hold Properties for at Least One Year

While holding properties for over a year doesn’t exactly eliminate your capital gains tax, it does change the nature of your capital gain. If you are flipping a property and buy and sell within a year, the gain will be a short-term capital gain. This means it will be taxed at the (typically) higher ordinary income tax rates. Holding it for

longer than a year means you will instead pay long-term capital gains rates which tend to be lower.

Strategy #2: Timing the Sale

Consider the timing of your sale to align with lower income years to potentially reduce your tax bracket.

What if you own a home which has increased in value over the years?

There are two strategies I recommend when it comes to your home:

Strategy #1: Take Advantage of the Primary Residence Exclusion

If you sell your primary residence, you may qualify to exclude up to $250,000 of capital gains from your income ($500,000 for married couples filing jointly) under IRC Section 121, provided you meet certain ownership and use tests.

Strategy #2: Keep records of capital improvements

Another strategy to reduce your capital gains tax is to simply keep good records of any capital improvements. These costs are added to your cost basis which reduces the amount of taxable gain you will incur when you sell the property. A capital improvement like replacing a roof, refinishing a kitchen or bathroom or adding an extension to your home can easily cost tens of thousands of dollars. It is important to make sure you get your full deduction on expenditures like this.

Can you save capital gains on rental income properties?

There is a wonderful opportunity to avoid the capital gains tax on the sale of rental property and defer the tax until another day by using a 1031 exchange strategy.

For investment properties, a 1031 exchange allows you to defer capital gains taxes by reinvesting the proceeds from a sale into a similar property. This is the best tax deferral strategy available to real estate investors.

This feature of the tax code enables someone to sell a property and then reinvest the proceeds in a qualifying replacement property without paying any tax. It does require the use of a 1031 intermediary and some planning in advance but is a common and powerful tactic for investors to use. Getting to reinvest the full proceeds from a sale into a new property enables you to earn much higher returns on one’s investment over time.

Can you avoid tax on appreciated stock?

There are three strategies on how to avoid the capital gains tax, beyond holding the stock for at least one year:

Strategy #1: Tax-Advantaged Accounts

Holding stocks in tax-advantaged accounts like IRAs or 401(k)s can defer taxes until withdrawal.

Strategy #2 Tax-Loss Harvesting

Offset gains with losses by selling underperforming stocks to reduce taxable income.

Strategy #3: Charitable Gifts

Donate a property that has increased in value. This allows you to permanently avoid paying tax on the growth. If you give the property to a friend or family member, they will eventually have to pay the tax themselves if or when they sell, but they still probably won’t complain!

If you give the property to a charity, either directly or through a Donor Advised Fund, you may also qualify for a significant charitable deduction.

But when is the right time to sell?

Don’t sell! If you have highly appreciated assets (such as your home or stocks) and you have to leave them to your loved ones (such as family) upon your demise, those assets receive a step up in basis to fair market value on the date of your death. Then, when they are sold, the capital gains are eliminated and only the appreciation after your death is subject to capital gains tax. This can result in a significant tax savings for your loved ones.

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Disclaimer: The information provided above is for general informational purposes only and is not legal advice.

Related Posts

Comments (0)