Whether you recently received one or are planning for the future, understanding how to keep…

Why is succession planning so critical for family businesses?

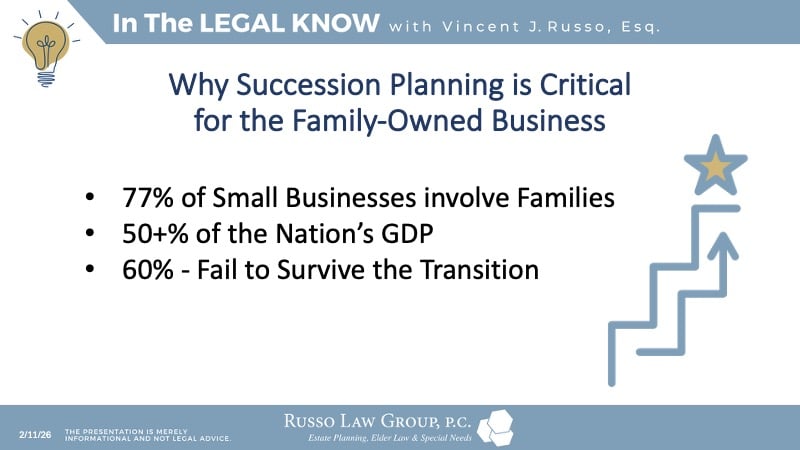

Family businesses are the backbone of our economy. A remarkable 77% of small businesses in the nation involve family members, highlighting their significant presence in the market.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/lWG6hfTpvAE

Their economic impact is substantial. Collectively, family-owned enterprises contribute over 50% of the United States’ Gross Domestic Product (GDP), demonstrating their vital role in national prosperity and stability.

Longevity requires a clear strategy. Without a formal succession plan, many of these valuable businesses do not survive the transition from one generation to the next. Proactive planning is essential to ensure the legacy and continued success of your business for years to come.

Longevity requires a clear strategy. Without a formal succession plan, many of these valuable businesses do not survive the transition from one generation to the next. Proactive planning is essential to ensure the legacy and continued success of your business for years to come.

In fact, 77% of small businesses involve families, and over half of the nation’s GDP is generated by family businesses. But many don’t survive past the second generation.

Succession planning is essential because it ensures the business can continue to thrive even as leadership transitions. Without a plan, families often face conflicts, financial instability, and even the loss of the business itself.

The success rate of family businesses surviving generational transitions is as follows:

- About 40% of family-owned businesses successfully transition to the second generation.

- Approximately 13% succeed to the third generation and only 3% are passed successfully to the fourth generation.

A lack of planning can also lead to family disputes, which can strain relationships and ultimately hurt both the family and the business. Succession planning helps avoid those conflicts by setting clear expectations and roles.

Ultimately, it’s about protecting the legacy and ensuring the business can support future generations.

What are common reasons family businesses fail?

The journey of a family business is filled with unique challenges. Without a solid framework for the future, several common pitfalls can unfortunately lead to failure.

Some of the biggest reasons include:

Lack of Communication

Communication is a major issue for families. When family dynamics and business discussions blur, misunderstandings can arise. A failure to establish formal communication channels often leads to unresolved conflicts and strategic misalignment.

Talking about succession often means addressing sensitive topics like retirement, death, or stepping aside. These are emotional conversations, and it’s easy for misunderstandings or hurt feelings to arise. That’s why it’s so important to approach these discussions with a clear plan and, in some cases, involve a neutral third party to facilitate.

Undefined Leadership Roles

Ambiguity over who is responsible for what can create power struggles and inefficiency. Without clearly defined roles and responsibilities, decision-making falters and accountability diminish.

Poor Financial Management

Merging family and business finances without strict policies is a frequent cause of trouble. A lack of professional financial oversight can result in cash flow problems, insufficient reinvestment, and ultimately, insolvency.

No Clear Successor

The absence of a designated and prepared leader for the next generation is a primary reason for failure. Without a clear succession plan, the business faces instability and a difficult, often unsuccessful, transition period when the current leader steps down.

Families can avoid these by formalizing roles, separating personal and business finances, and having open, honest discussions about the future.

What does a good succession plan look like?

Securing the future of your family business requires proactive strategy and clear execution. Here are the essential steps to building a robust plan:

Identify and Train a Successor

Start early by pinpointing potential leaders within the family or organization. Once identified, one should invest heavily in their professional development through mentorship, training programs, and gradually increasing responsibilities to ensure they are ready to lead.

Formalize Leadership Roles

Move away from informal understandings. Create clear, written job descriptions and organizational charts that define authority and accountability. This clarity reduces conflict and ensures everyone understands their specific contribution to the company’s success.

Separate Personal and Business Finances

Implement strict financial discipline by keeping household expenses distinct from company accounts. Establishing this boundary is crucial for accurate financial reporting, tax compliance, and maintaining the professional integrity of the business.

For example, I’ve seen families struggle when personal finances get mixed with business finances. By keeping these separate and setting clear boundaries, they were able to reduce conflict and focus on growing the business.

Hold Regular Family Meetings

Establish a formal schedule for family business meetings. These gatherings provide a structured forum to discuss business performance, address family dynamics, and ensure all stakeholders are aligned on the vision and strategy for the future.

It’s also important to involve the family in the process and get professional guidance to ensure all bases are covered. Families should start early and create a roadmap for the company’s future.

The earlier, the better. Ideally, you should start planning as soon as the business is established. But if you haven’t started yet, don’t worry – it is never too late to begin. Creating a timeline is critical so that the family keeps on track to ensure a smooth handoff.

What to avoid when planning for succession?

Even the most well-intentioned succession strategies can falter if key elements are overlooked. Steering clear of these frequent errors is essential for a smooth transition. Some common mistakes include:

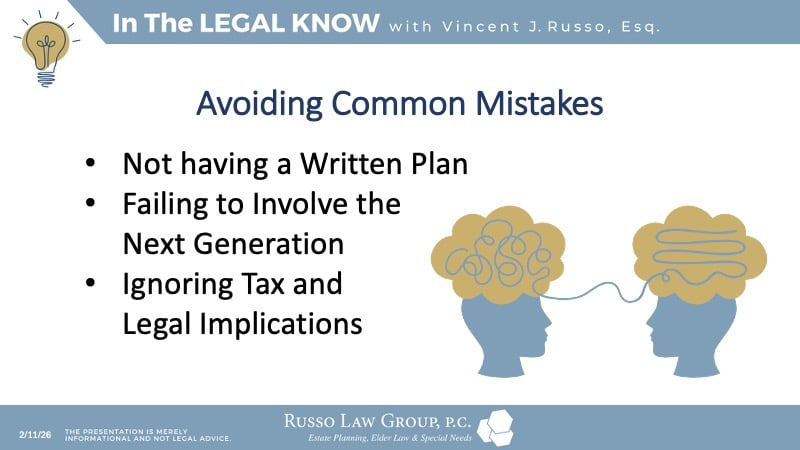

Not Having a Written Plan

A verbal understanding is simply not enough. Without a formal, documented roadmap, details get lost and memories fade. You must commit the plan to a writing to serve as the definitive guide, ensuring clarity and preventing disputes among family members when the time comes to execute the transition.

Failing to Involve the Next Generation

Succession is a shared journey, not a surprise announcement. If you exclude future leaders from the planning process, they may lack the necessary buy-in or understanding of the company’s vision. engaging them early fosters a sense of ownership and allows them to prepare for the weight of leadership.

Ignoring Tax and Legal Implications

Transferring ownership is a complex legal and financial event. If you fail to account for estate taxes, gift taxes, and legal structures, the financial burden could be devastating. Proper planning with professionals is required to preserve the wealth you have built and ensure that the proper path has been taken from a tax and legal standpoint.

Addressing legal and financial considerations may also include updating wills, trusts, and business agreements. Avoiding these mistakes can save families a lot of stress and ensure a smoother transition.

When the transition is not working, consider bringing in an unbiased third party, like a mediator or advisor, to help facilitate discussions and keep things on track.

If you would like to speak with an experienced elder law attorney regarding your situation or have questions about something you have read, please do not hesitate to contact our office at 1 (800) 680-1717. We look forward to the opportunity to work with you.

Disclaimer: The information provided above is for general informational purposes only and is not legal advice.

Related Posts

Comments (0)