Learn about ABLE accounts and how they help individuals with disabilities save without losing essential benefits.

What is an ABLE account?

An ABLE account, which stands for Achieving a Better Life Experience, is a tax-advantaged savings account.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/kxiSEMIr-cQ

It allows individuals who became disabled before the age of 46 and their families to save money for disability-related expenses.

The key benefit is that funds in an ABLE account generally do not count against the asset limits for needs-based government benefits like Supplemental Security Income, or SSI, and Medicaid.

This protects eligibility for those vital programs while allowing for more financial security.

Key Details and Requirements

- Eligibility: The disability must have occurred before age 46 (as of January 1, 2026). Individuals already receiving SSI or SSDI automatically meet the disability requirement.

- Contribution Limits: In 2026, annual contributions are limited to $20,000 (from all sources).

ABLE to Work: Working beneficiaries may contribute additional funds from their earnings. If you work and don’t contribute to a 401(k) or 403(b), you can add earned income up to the prior year’s poverty line (approximately $15,000 for 2026 in the 48 contiguous states and District of Columbia.

- Tax Benefits: Earnings on contributions grow tax-free, and withdrawals are tax-free if used for qualified expenses.

- Qualified Expenses: These include education, housing, transportation, employment training, assistive technology, personal support services, and health/prevention services.

- Opening an Account: Accounts are state-administered, but you can choose a plan from a different state; most can be opened online.

- One Account: Only one ABLE account is allowed per person

It is important to point out that there has been a significant change in the age requirement prior to January 1, 2026, it was age 26 and now it is age 46 under the ABLE Age Adjustment Act.

It is important to point out that there has been a significant change in the age requirement prior to January 1, 2026, it was age 26 and now it is age 46 under the ABLE Age Adjustment Act.

There is also a Lifetime Limit on the account balance in an ABLE Account: total account balances (contributions + earnings) can reach roughly $235,000 to over $500,000 depending on the State, but SSI benefits are suspended if the balance exceeds $100,000.

What are the key benefits of an ABLE Account?

The key benefits of an ABLE Account are:

- Protects Government Benefits

- Tax-Advantaged Savings

- Financial Independence

What expenses qualify for “disability-related expenses.”?

It’s a very broad category, which is one of the strengths of the program.

Qualified disability expenses (QDE) are expenses made for the benefit of the designated beneficiary and related to his or her disability, including, but not limited to:

- Education;

- Housing;

- Transportation;

- Employment training and support;

- Assistive technology and related services;

- Health;

- Prevention and wellness;

- Financial management and administrative services;

- Legal fees;

- Expenses for ABLE account oversight and monitoring;

- Funeral and burial; and,

- Basic living expenses.

The goal is to help the individual maintain or improve their health, independence, and quality of life.

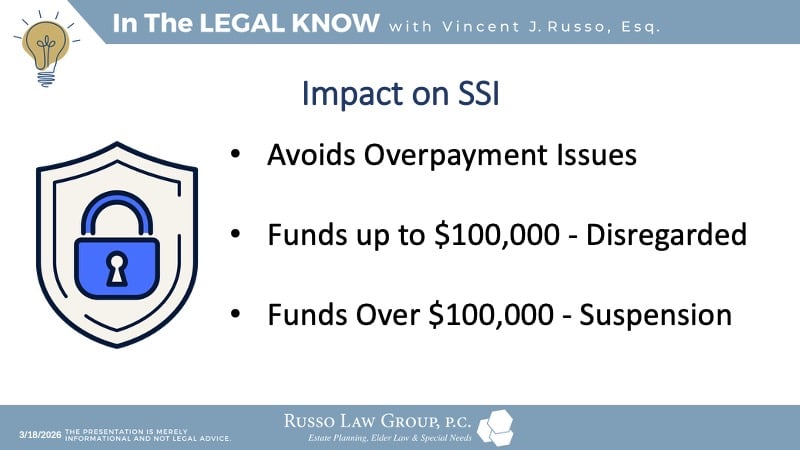

How does an ABLE account specifically interact with SSI?

For SSI recipients, the first $100,000 in an ABLE account is completely disregarded as a resource.

This is a game changer, as the normal SSI asset limit is just $2,000 for an individual. This means a person can have substantial savings for their needs without losing their monthly SSI payments.

However, it’s important to note that if the ABLE account balance exceeds $100,000, SSI payments will be suspended until the balance drops back below that threshold, though Medicaid eligibility is not affected.

There is also the benefit of dealing with Overpayments and SSI.

Overpayments can happen if an SSI recipient receives an inheritance, a gift, or back-payments from Social Security that push their assets over the $2,000 limit. If that money is not spent down in the same calendar month it’s received, SSI will issue an overpayment notice and seek to claw back benefits.

By transferring those funds into an ABLE account, the individual can preserve the money for future use without disrupting their SSI eligibility and avoid the stress of an overpayment situation.

How do ABLE Accounts grow tax-free?

The money contributed to an ABLE account can be invested, and any growth or earnings on those investments are not subject to federal and state income tax. Furthermore, when the money is withdrawn to pay for those qualified disability expenses we discussed, the withdrawals are also tax-free. This allows the savings to grow more effectively over time.

What happens if someone’s disability begins later in life?

That’s a great question. The age 46 requirement is a strict rule for opening an ABLE account. For individuals whose disability occurred later or for those who don’t qualify for other reasons, there are other planning tools. The most common is a Special Needs Trust. These trusts serve a similar purpose of holding assets for the benefit of a person with a disability without compromising their eligibility for government benefits.

The rules are different, so it’s a good idea to discuss which option is the best fit for a specific situation.

What happens to the money in an ABLE account if the individual passes away? Is it subject to Medicaid recovery?

This is an important consideration. After the individual’s death, some states can file a claim against the remaining funds in an ABLE account to recoup Medicaid payments made on behalf of the individual. This is known as Medicaid payback or recovery.

However, this only happens after any outstanding qualified disability expenses have been paid. The rules can vary by state, so it’s something to be aware of.

CLICK HERE for the complimentary Russo Law Group Special Needs Planning Guide.

If you would like to speak with an experienced elder law attorney regarding your situation or have questions about something you have read, please do not hesitate to contact our office at 1 (800) 680-1717. We look forward to the opportunity to work with you.

Disclaimer: The information provided above is for general informational purposes only and is not legal advice.

Related Posts

Comments (0)