April 15th is Tax Day! Learn essential tips for your tax return to avoid common errors and ensure timely processing.

The Silver Tsunami is the wave of Baby Boomers entering their senior years—and with it, a massive increase in the demand for long term care. The question is: are we ready?

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/mUrGKFJ5NOE

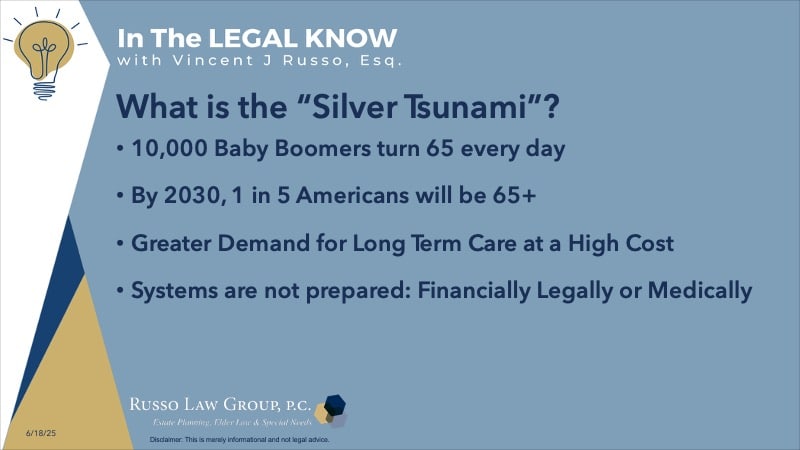

What is the “Silver Tsunami” and how does it impact long term care needs?

The “Silver Tsunami” refers to the aging of the Baby Boomer generation—roughly 10,000 people a day turning 65.

By 2030, 1 in 5 Americans will be over 65 which means we are facing a massive demographic shift. People are living longer, and as we age, many of us will need help with everyday activities like bathing, dressing, or managing medications. This kind of care—known as long-term care—can be provided at home, in assisted living, or in nursing homes.

But here’s the catch: it’s extremely expensive, and most people don’t have a plan. The average nursing home costs are in the area of $111,000 per year. In California the average cost is $144,000 per year and in New York State, the annual cost generally ranges from $100, 000 to $180,000.

Our systems—financial, legal, and healthcare—aren’t fully prepared.

What are the biggest misconceptions people have about long-term care coverage?

A lot of folks assume Medicare or private health insurance will take care of long-term care. Unfortunately, that is one of the biggest myths.

Medicare covers only short-term rehab, under strict conditions—and usually no more than 100 days. It does not cover long-term custodial care. Private insurance also generally excludes it.

Many older adults then rely on Medicaid which has strict eligibility rules and may require families to spend down assets. Without a plan, families often face out-of-pocket costs that can drain life savings.

When should someone start planning for long term care—and what are the legal tools available?

The key is planning ahead—while you’re still healthy and able to make decisions. Ideally, people should start planning in their 50s or early 60s—before a health crisis hits.

From a legal perspective, key tools include:

- A Durable Power of Attorney for financial decisions

- Medical Directives such as a Health Care Proxy and Living Will for medical wishes

- And one of the most powerful: a Medicaid Asset Protection Trust, which helps preserve assets like the family home while still qualifying for long-term care benefits

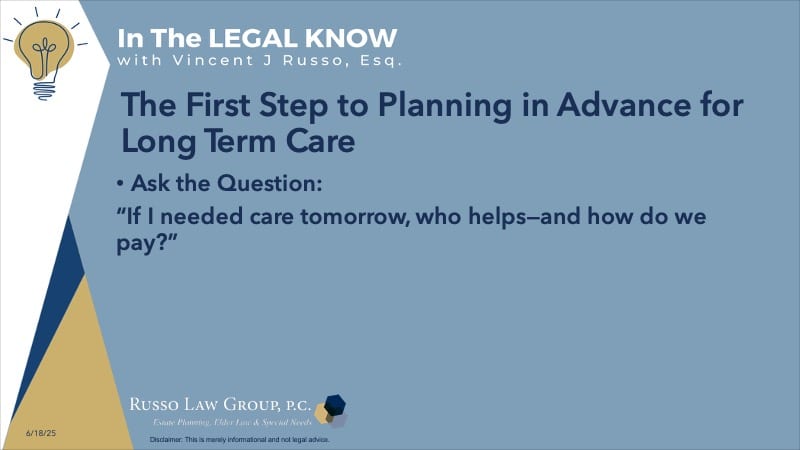

What’s the very first step?

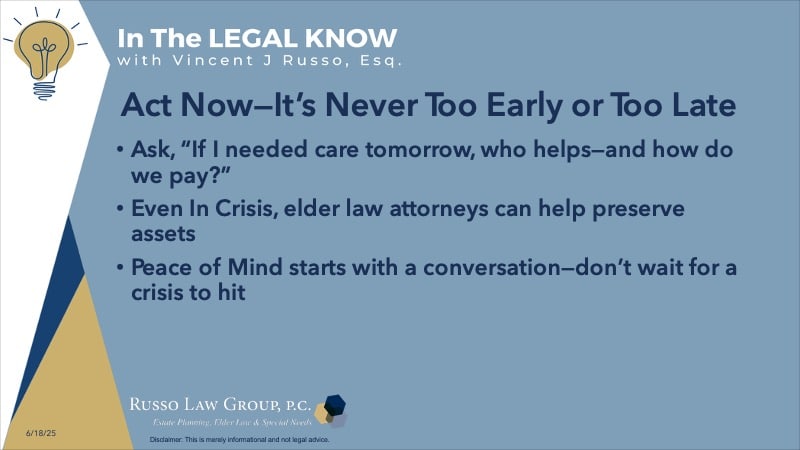

Start by asking yourself: “If I needed care tomorrow, who would help me—and how would we pay for it?”

If you don’t have a clear answer, it is time to speak with an elder law attorney. Elder law attorneys can create a plan that protects your independence, your savings, and your loved ones.

Planning ahead gives you choices, and it prevents your family from having to make tough decisions under pressure.

A team approach is best: seek professional advice and consult with financial the elder law attorney, financial advisor and healthcare professionals to develop a tailored plan.

What happens if someone didn’t plan ahead—are there still options?

It’s never too late to do something!

Even in crisis, a qualified elder law attorney can help protect some (if not all) of the assets, apply for Medicaid correctly, and reduce the financial blow. But the options are fewer, and the stress is greater. That’s why planning ahead is such a gift to your family.

Don’t wait for a health crisis to force your hand. The Silver Tsunami is real, but with good planning, it doesn’t have to drown your future. If you want peace of mind, start the conversation now.

Whether you’re in your 50s, 60s, or helping aging parents—it’s never too early, and never too late, to plan ahead. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Disclaimer: The information provided above is for general informational purposes only and is not legal advice.

Related Posts

Comments (0)