This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/aQgwbQkJtC0 How can SSI…

Vincent Russo on CFN Live – Medicaid Home Care: Protecting Your Income

Vea a Vincent J. Russo como corresponsal jurídico en el programa CFN Live de Catholic Faith Network.

Vincent appeared on CFN Live on Marzo 1st to discuss

“Medicaid Home Care: Protecting Your Income”

Colleen: Today, we will be addressing Part Two in our Series on “Trusts and Medicaid” with Vincent J. Russo “In the Legal Know”.

Vincent:

Colleen, great to be here, last week we addressed how critical it is for seniors to plan for Medicaid long term care services.

Trusts can play an important role in protecting one’s assets while accessing Medicaid.

Last week, I addressed how to protect one’s residence by utilizing the Medicaid Asset Protection Trust while accessing Medicaid home care or nursing home care services.

Today, we will address how to protect one’s income while on Medicaid home care.

Colleen: Vincent, can you first explain again why Medicaid home care is so vital?

Vincent:

Medicaid home care is so vital because Medicaid does not cover home care services.

Colleen: Now, I understand that once you are eligible for Medicaid home care, there is a Medicaid income budget rule, how does that work.

Vincent:

Once you meet the criteria for assistance with activities of daily living and the asset test, you are approved for Medicaid home care.

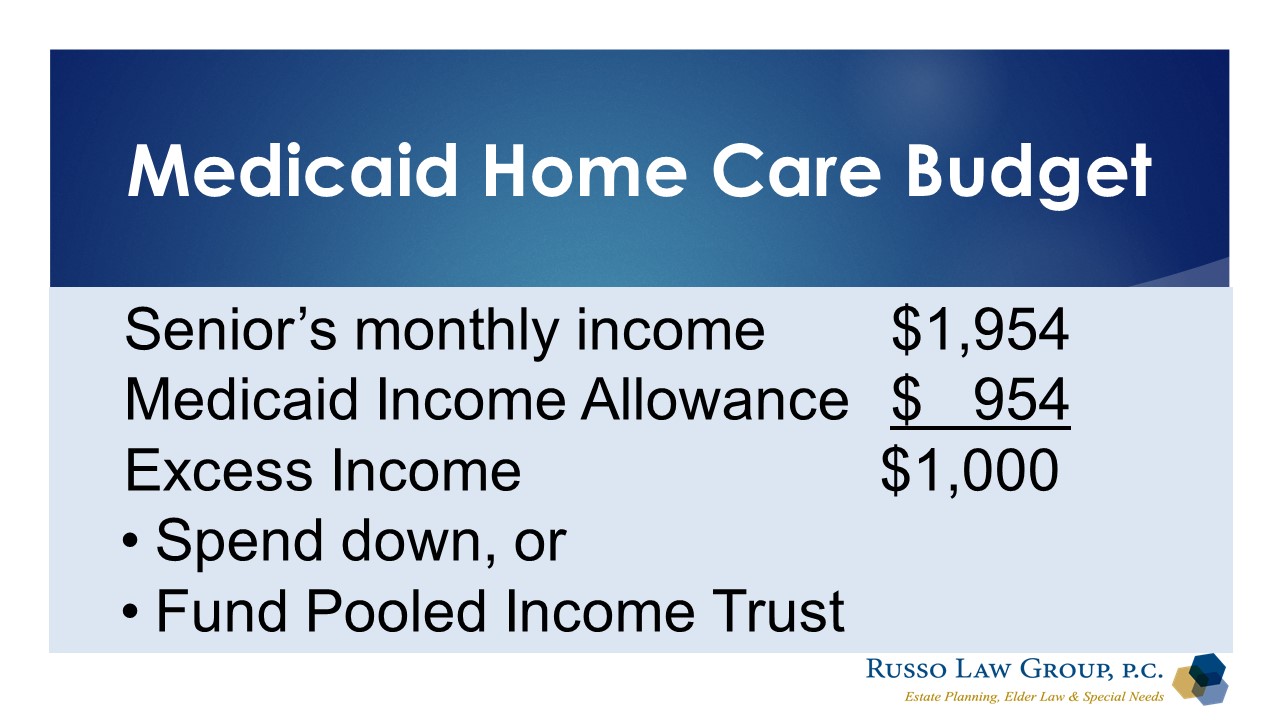

But there is one more step, Medicaid will take a look at your monthly income. If you have more than $954, then Medicaid (which is a payer of last resort) says you have to spend down that excess income before they will pay for the services.

For example, if the senior has $1,954 of monthly income and the income allowance is $954, the senior is allowed to keep $954 and the balance ($1,000) would have to spent down. Of course, we know that seniors cannot live on $954 per month.

For example, if the senior has $1,954 of monthly income and the income allowance is $954, the senior is allowed to keep $954 and the balance ($1,000) would have to spent down. Of course, we know that seniors cannot live on $954 per month.

Colleen: what if you are married, then how does it work?

Vincent:

Then, we have another set of rules that will allow the married couple up to $3,425 each month to live on. If the income is higher, then a Pooled Trust or spousal refusal (which we can discuss another day) can help protect the excess income.

Now for the solution:

The excess monthly income can go into a Pooled Income Trust in NY and then that income can be spent on the living expenses of the senior without having to be spent down each month.

This will allow the senior to be able to remain at home and receive the care he or she needs covered by Medicaid.

Colleen: How does it work?

Vincent:

Each month, the senior would contribute his or her excess income to the Pooled Trust (a separate subaccount would be set up), then the senior would submit bills for his or her living expenses and the Pooled Trust would pay the bills.

If there are any funds remaining in the account, those funds would pass to the Charity which created the Trust.

There are over 22 Pooled Trusts in New York and one of them is the Theresa Pooled Trust.

The Theresa Foundation was established by my family in memory of my daughter, Theresa and the Foundation supports music, dance, art, and recreation for children with special needs.

Colleen: This is an awfully complicated way to provide long-term care for our seniors. What should seniors do about this?

Vincent:

Planning in advance and getting the right advice is the key.

No one should lose their life savings because they have long-term care needs.

Colleen: Vincent, what comes next?

Vincent:

Next week, we will discuss the use of trusts for people under 65 who need Medicaid and SSI- Supplemental Security Income.

Si desea más información sobre estos temas y otros, puede descargar gratuitamente nuestras Guías de planificación desde el sitio web de nuestro bufete, vjrussolaw.com.

Puede encontrar a Vincent en episodios anteriores de CFN Live haciendo clic aquí.

Los temas incluyen:

- Cambios en el programa de atención domiciliaria de Medicaid del Estado de Nueva York

- Conceptos básicos de planificación patrimonial - Parte 1: ¿Por qué necesito un plan de sucesión?

- Conceptos básicos de planificación patrimonial - Parte 2: ¿Qué incluye un plan patrimonial?

- Conceptos básicos de planificación patrimonial - Parte 3: ¿Cuándo y por qué debo actualizar mi plan patrimonial?

- Planificación patrimonial para niños con necesidades especiales - Parte 1: ¿Cómo cuido y protejo a mi hijo?

- Planificación patrimonial para niños con necesidades especiales - Parte 2: ¿Qué prestaciones públicas existen?

- Planificación patrimonial para niños con necesidades especiales - Parte 3: ¿Qué medidas debo tomar para mi hijo adulto con necesidades especiales?

- Planificación de la asistencia a largo plazo - Parte 1: "¿Cómo pago la asistencia a largo plazo?"

- Planificación de la asistencia a largo plazo Parte 2: "¿Cómo puede ayudarme la asistencia domiciliaria de Medicaid?"

- Planificación de la asistencia a largo plazo - Parte 3: "Cómo cumplir los requisitos para Medicaid"

- ¿Qué es un poder notarial?

- Actualizaciones jurídicas importantes

Esperamos que sintonice CFN Live. Es un programa dinámico con noticias de actualidad y colaboradores fascinantes que tienen historias inspiradoras que contar. El nuevo programa CFN Live se emite de lunes a viernes. a las 9 de la mañana y a las 7 de la tarde. Podrá ver el programa en cualquier momento, según le convenga, en el canal de YouTube de CFN.

a las 9 de la mañana y a las 7 de la tarde. Podrá ver el programa en cualquier momento, según le convenga, en el canal de YouTube de CFN.

Puede obtener más información sobre la Red de Fe Católica y CFN Live visitando https://www.catholicfaithnetwork.org/cfn-live.

Socio Director de Russo Law Group, Vincent J. Russoes uno de los principales colaboradores del nuevo programa CFN Live de Catholic Faith Network. Vincent es el corresponsal jurídico del programa. En su segmento, titulado "In the Legal Know", Vincent le mantendrá al tanto de las últimas novedades legales, incluyendo la ley de ancianos, necesidades especiales y planificación patrimonial - todo para ayudarle a tomar decisiones de planificación informadas para protegerse a sí mismo, a sus seres queridos y a sus activos.

Socio Director de Russo Law Group, Vincent J. Russoes uno de los principales colaboradores del nuevo programa CFN Live de Catholic Faith Network. Vincent es el corresponsal jurídico del programa. En su segmento, titulado "In the Legal Know", Vincent le mantendrá al tanto de las últimas novedades legales, incluyendo la ley de ancianos, necesidades especiales y planificación patrimonial - todo para ayudarle a tomar decisiones de planificación informadas para protegerse a sí mismo, a sus seres queridos y a sus activos.

Entradas relacionadas

Esta entrada tiene 0 comentarios