Abril 15th is Tax Day! Learn essential tips for your tax return to avoid common errors and ensure timely processing.

Many people do not realize that Medicaid can recover costs from your estate after you pass away. Moreover, it can have a significant impact on your family’s financial future.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/lEY07woz3bI

Medicaid is often the key to receiving vital long-term care for seniors. However, the rules are overly complex and can vary state by state. One part of the Medicaid program that people may not be aware of is “Medicaid Estate Recovery.” This process can be devastating to families who are blindsided by this government recovery program.

What is Medicaid Estate Recovery?

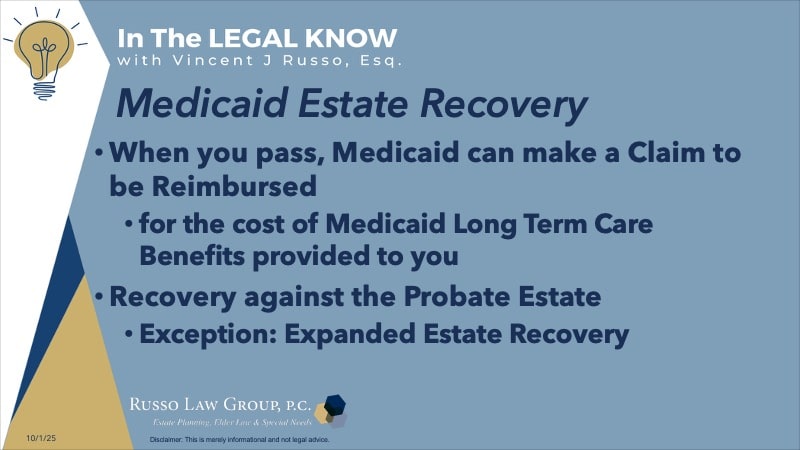

Medicaid Estate Recovery is a process where Medicaid seeks to recover the costs it paid for a recipient’s care from their estate after they pass away. This includes expenses like nursing home care, home health care, and other services covered by Medicaid. Essentially, Medicaid is reimbursing itself for the benefits it provided during the recipient’s lifetime.

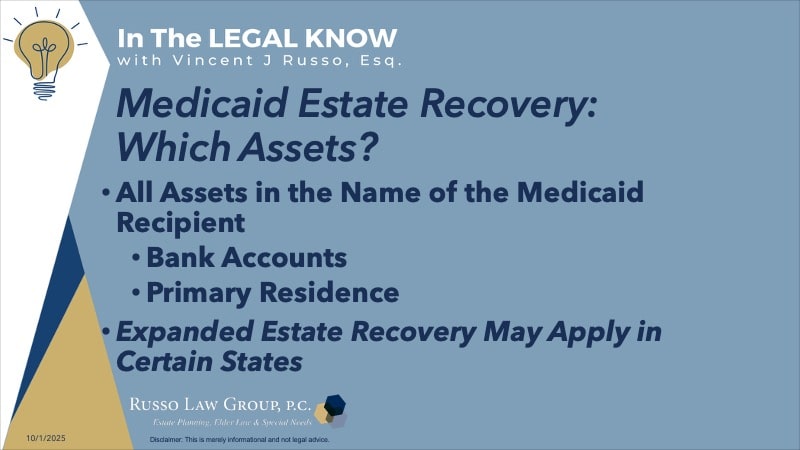

All U.S. states have mandatory Medicaid Estate Recovery programs that allow them to seek reimbursement from a deceased Medicaid recipient’s estate for certain long-term care costs. However, the scope of these programs varies significantly by state. For example, some opt for broader recovery (sometimes referred to as “Expanded Estate Recovery”) while others have more robust protections for surviving family members.

In effect, some states can recover from non-probate assets like joint tenancies, or living trusts. Others are limited to assets that pass through the probate process.

Many people are shocked to learn that this could happen, especially if they thought Medicaid was a free benefit. It is more like a loan that Medicaid can collect later. And that is why planning is so important. With proper planning, Medicaid estate recovery can be avoided.

Who is subject to Medicaid Estate Recovery?

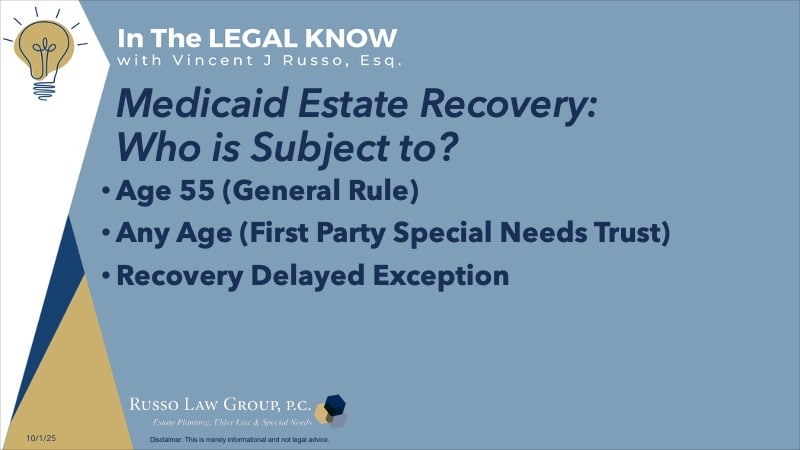

Not everyone is subject to Medicaid Estate Recovery. Medicaid Estate Recovery typically applies to individuals who were 55 or older when they received Medicaid benefits such as:

- Nursing facility services

- Home and community-based services

- Related hospital and prescription drug services

However, there are exceptions that are more or less restrictive than the general rule. For instance, recovery can be made regardless of age against the trust assets in a First Party Special Needs Trust.

In addition, if the recipient has a surviving spouse, a minor child, or a blind or disabled child, Medicaid may not pursue recovery immediately. But once those exceptions no longer apply, recovery can proceed.

When and how does Medicaid recover from an estate?

Medicaid can only recover after the recipient has passed away, and the recovery may be limited to assets that are part of the probate estate (subject to your state laws). This means assets that are solely in the recipient’s name at the time of death. For example, if someone owns a home jointly with a spouse or has assets in a trust, those assets may not be subject to recovery. However, if the assets are in the recipient’s name alone, Medicaid can file a claim against the estate during the probate process.

Medicaid typically has a limited window to file a claim, which varies by state. In New York, for example, Medicaid must file its claim during the probate process, which usually begins shortly after the recipient’s death. Therefore, this is why it is so important to have a plan in place before it’s too late.

Are all assets subject to recovery? What about my home?

You may be thinking if I am on Medicaid how do I have any assets subject to Medicaid estate recovery? Medicaid can recover from assets like bank accounts, real estate, and other property in the probate estate. Your home is often a key target for recovery because it is usually one of the most valuable assets in an estate. However, there are exceptions:

Typically, there are two assets that Medicaid will seek to recover against: a bank account which has funds below the Medicaid resource allowance and your home (if you lived in it or had an intent to return home).

For example, let’s say Mary, a 75-year-old widow with three adult children, resided in New York and received Medicaid benefits to cover her nursing home care for the last three years of her life. After Mary passed away, Medicaid filed a claim against her estate to recover $300,000 in benefits paid for her care.

Mary’s home, valued at $300,000, was part of her probate estate because it was solely in her name. Since there are no exemptions—like a surviving spouse or disabled child—Medicaid can place a lien on the property. The home is then sold, and the entire $300,000 from the sale must go to Medicaid. As a result, Mary’s children are left with nothing.

How can someone avoid Medicaid Estate Recovery?

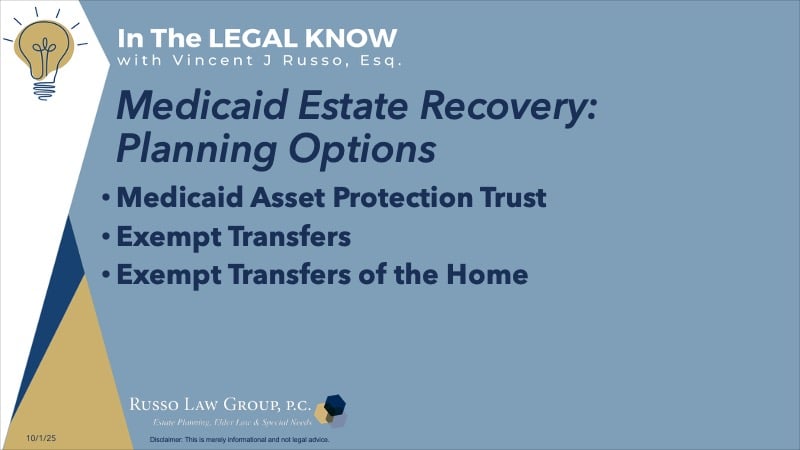

The Medicaid estate recovery rules are complicated. With proper planning, you can protect your assets. Knowing the rules and planning can help protect your assets and your family’s financial future. Strategies like creating a Medicaid Asset Protection Trust, transferring assets in advance, or ensuring certain exemptions apply can help.

For example, placing your home in a Medicaid Asset Protection Trust can remove it from your probate estate, making it inaccessible to Medicaid recovery (subject to state law). It is also important to act early. This is because Medicaid has a five-year look-back period for asset transfers. This means any transfers made within five years of applying for Medicaid could be penalized.

In our example, in New York, if Mary had placed her home in a Medicaid Asset Protection Trust five years before applying for Medicaid, it would not have been part of her probate estate, and Medicaid would not have been able to recover from it. In my example, Mary’s children would have received the entire $300,000 when the home was sold. Planning ahead is key.

There are also exceptions to the Medicaid transfer penalty rule for assets and for a home. This would allow an individual to make certain transfers and still qualify for Medicaid while avoiding a Medicaid estate recovery.

Exempt Medicaid asset transfers include gifts to a spouse, a disabled child, or a minor child, as well as transfers to a trust for the sole benefit of a disabled individual under age 65.

When a primary residence is involved, the home could be transferred during lifetime without a Medicaid transfer penalty to the following individuals: your spouse, a child under 21, a blind or disabled child, a caregiver child (who lived with you for two years and provided care), or a sibling with an equity interest who has lived there for one year before your institutionalization.

For example: John, an 80-year-old man, lives in his home with his daughter, Sarah, who has cared for him for several years. John now needs Medicaid to cover his nursing home care.

Because Sarah had lived in his home and provided care for at least two years before John entered the nursing home, the home was exempt from the Medicaid transfer penalty rule and thus, avoided Medicaid Estate Recovery. Sarah was able to keep the home without Medicaid placing a lien on it.

Unfortunately, long term care is expensive and not covered by Medicare. The cost of care can wipe out a lifetime of savings. Then, on top of that, you could lose your home to Medicaid estate recovery. My advice is to start early and meet with an experienced elder law attorney who can guide you. The earlier you start planning, the more options you’ll have to protect your assets and your family’s financial future.

If you would like to speak with an experienced elder law attorney regarding your situation or have questions about something you have read, please do not hesitate to contact our office at 1 (800) 680-1717. We look forward to the opportunity to work with you.

Disclaimer: The information provided above is for general informational purposes only and is not legal advice.

Entradas relacionadas

Comments (0)