Discover the nuances of ownership in condos versus coops. Tune in to Vincent J. Russo for essential insights.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/mApEWD5MFzc

What is the fundamental difference between owning a condo and owning a co-op?

When you purchase a condo, you are buying real property —you receive a deed, just like you would with a house.

When you purchase a condo, you are buying real property —you receive a deed, just like you would with a house.

With a co-op, however, you are purchasing shares in a corporation that owns the building, and in return, you receive a proprietary lease to your unit. This difference impacts everything from financing to day-to-day living.

In a condo setting, there is more flexibility as to financing and subletting while in a Co-op setting, there is less flexibility as there may be board approvals required and restrictions on what you can do with your apartment.

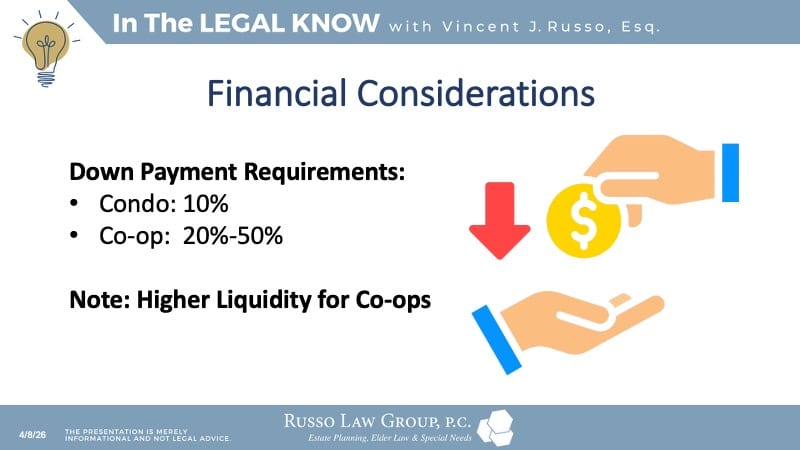

What are some of the key differences in terms of down payments and financial requirements?

Typically, the purchase price of a Co-op is less than the purchase price for a comparable condo. The difference could be up to 40% less. Meanwhile, Condos offer more flexibility as to financing.

Financing is simpler, and down payments can be as low as 10%. Co-ops, on the other hand, often require higher liquidity and down payments ranging from 20% to 50%.

Additionally, co-op boards may have strict financial requirements for approval.

How does the approval process differ between condos and co-ops?

Co-op boards are typically much stricter. They can require interviews, financial disclosures, and even references.

Condos, while they may have some rules, generally have a more straightforward approval process.

What are the restrictions for renting out a unit in a condo versus a co-op?

Condos are more flexible when it comes to subletting. You can often rent out your unit freely. Co-ops, however, tend to have strict subletting policies, often limiting the number of years you can rent out your unit or requiring board approval.

For co-ops, how much of the monthly maintenance fee is tax-deductible?

A portion of the co-op’s monthly maintenance fee, which includes property taxes and mortgage interest, is often tax-deductible.

The exact amount depends on the building’s financials, so it is important to review those details carefully.

In a condo setting, you can deduct property taxes and mortgage interest directly related to the condo property.

It is important to note that deductibility of taxes is limited to the SALT cap (up to $40,000 if you meet certain requirements).

For a primary residence, you generally cannot deduct monthly condo or HOA fees as they are considered personal living expenses.

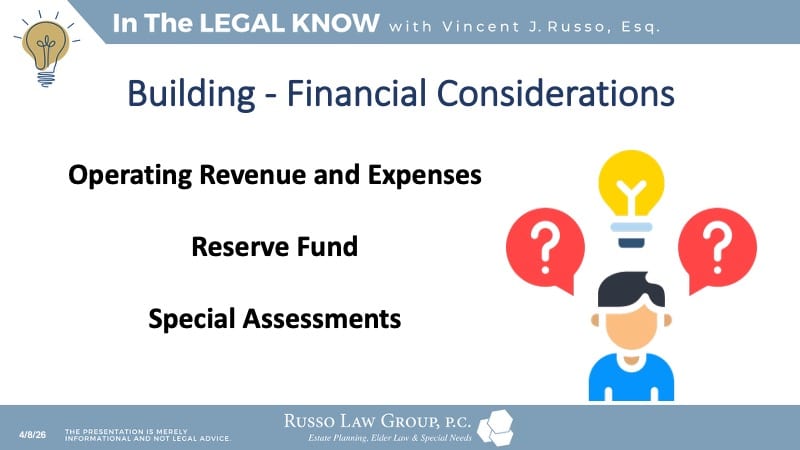

What should buyers look for when reviewing a building’s financials?

Buyers should ask for the building’s financial statements and look at the reserve fund.

A healthy reserve fund is critical for covering unexpected repairs or maintenance.

It is also important to check for any planned special assessments, which are additional fees that may be charged to cover major projects like roof repairs or façade work.

What are some lifestyle considerations buyers should think about?

Lifestyle plays an important role!

For example, co-ops often have stricter rules about pets, renovations, and even who can live in the unit. Condos tend to be more flexible, which can be appealing to people who value freedom and flexibility. It really depends on what’s most important to the buyer.

Condos are easier to sell or rent out, making them a better option for people who might need to relocate. Co-ops, with their stricter rules and approval processes, can be more challenging to sell or sublet quickly.

Vincent J. Russo’s Key Advice

My advice is to do your homework. Review the condo development or building’s financials, understand the rules and policies, and think about your long-term goals.

And do not hesitate to consult with professionals, whether it is a real estate attorney or a financial advisor, to make sure you’re making the best decision for your situation.

If you would like to speak with an experienced elder law attorney regarding your situation or have questions about something you have read, please do not hesitate to contact our office at 1 (800) 680-1717. We look forward to the opportunity to work with you.

Disclaimer: The information provided above is for general informational purposes only and is not legal advice.

Entradas relacionadas

Comments (0)