Find out how an ABLE account can enhance financial security and provide essential support for those with disabilities.

A UTMA account, created under the Uniform Transfers to Minors Act (UTMA), lets minors receive and hold gifts such as money, real estate, fine art, and other assets without needing a formal trust. Usually, a parent or guardian acts as custodian and manages the account until the child reaches the age of majority in their state. At that time, the child gains full control over the assets.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/J9aMrXcKEO8

Table of Contents

How Does a UTMA Account Work?

In a UTMA account, an adult—often a parent or guardian—acts as the custodian. The custodian has full control over the account and can make investment decisions on behalf of the minor. The custodian manages the account for the benefit of the minor and can withdraw funds as needed for the child’s benefit. Once the child reaches the age of majority, the assets are transferred to their control.

The custodian can withdraw and use the UTMA funds for expenses that benefit the child. These expenses can include:

-

Educational costs

-

Medical expenses

-

Other needs related to the child’s well-being

However, the funds must be used in a manner that benefits the minor.

Anyone can contribute to a UTMA account, but their contribution is considered an irrevocable gift. This means only the custodian has the right to withdraw funds, and it must be for the child’s benefit. The custodian has a fiduciary duty to act in the child’s best interest.

When Can the Child Withdraw UTMA Funds?

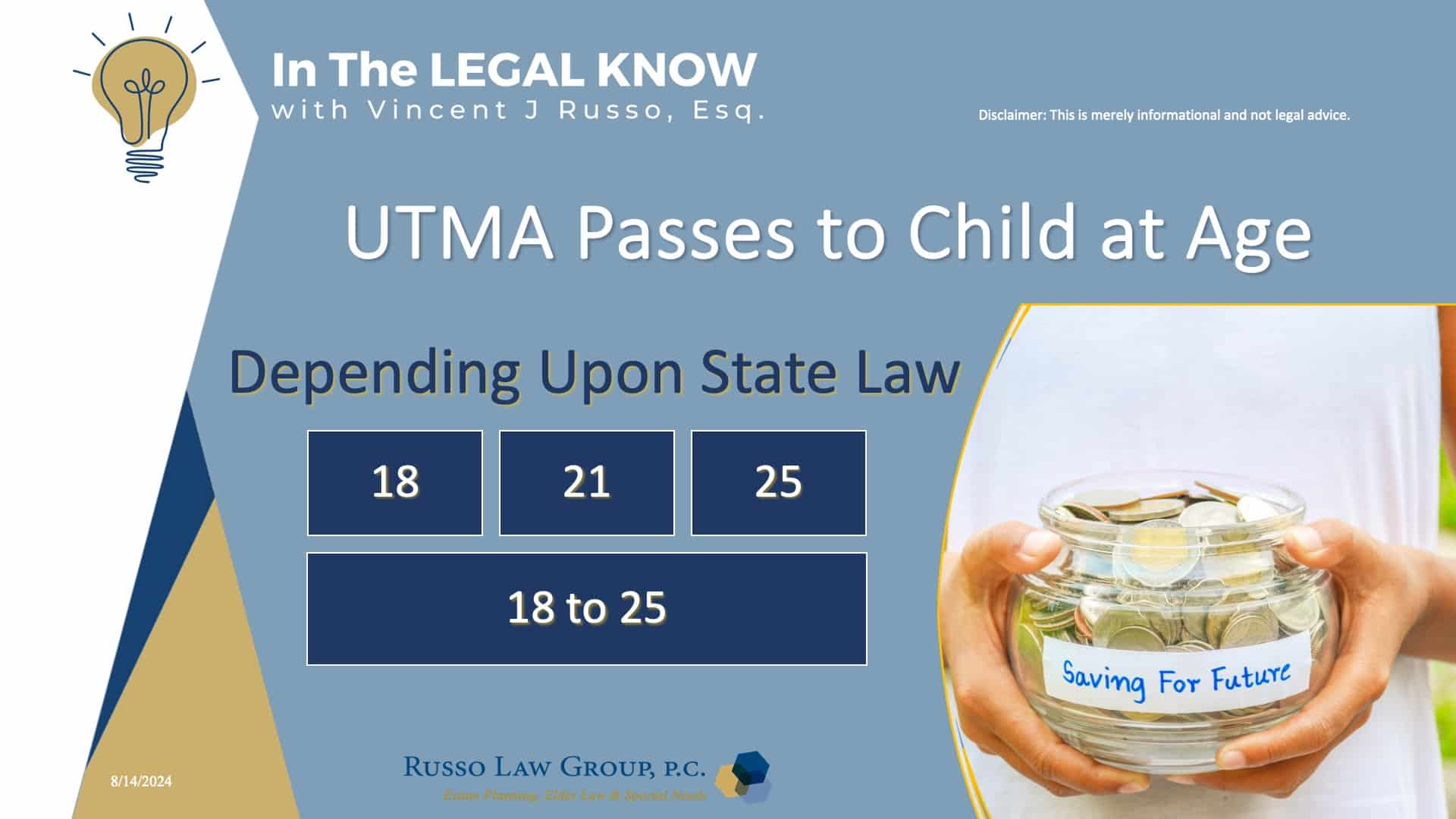

The child can access and withdraw the UTMA funds once they reach the age of majority as defined by their state’s law.

Depending on the state, a UTMA account is handed over to a child when they reach either age 18 or age 21. In some jurisdictions:

-

At age 18, a UTMA account can only be handed over with the custodian’s permission.

-

At age 21, the account is transferred automatically.

Likewise, an adult can elect to maintain custodianship over the assets until the beneficiary reaches up to age 25, depending on the state in which the account exists. The custodian can sometimes choose between a selection of ages.

For example:

-

In New York, the UTMA generally requires the custodian to transfer the custodial property to the minor when the minor reaches age 21, unless the person creating the account elects the age of 18 instead.

-

In Florida, you can set up an UTMA that ends when the child reaches any age between 21 and 25. You get to decide the precise age the beneficiary gains access to the assets. However, if you choose an age over 21, the custodian must allow the beneficiary to take ownership within one month of their 21st birthday.

-

In Virginia, the custodian can decide whether the beneficiary gets control of the account assets at age 18, 21, or 25.

| Estado | Default Age of Transfer | Options / Notes |

|---|---|---|

| Nueva York | 21 | Custodian must transfer at 21 unless account creator elects transfer at 18 |

| Florida | 21 to 25 (custodian selects) | If over 21, beneficiary must be allowed control within one month after 21st birthday |

| Virginia | 18, 21, or 25 (custodian selects) | Custodian decides exact age of transfer |

The key takeaway here is simple: when the child in your life comes of age, everything in the UTMA custodial account you’ve created for them becomes their legal property. That’s why it’s crucial to fully understand your state’s rules and prepare children for this transfer of assets.

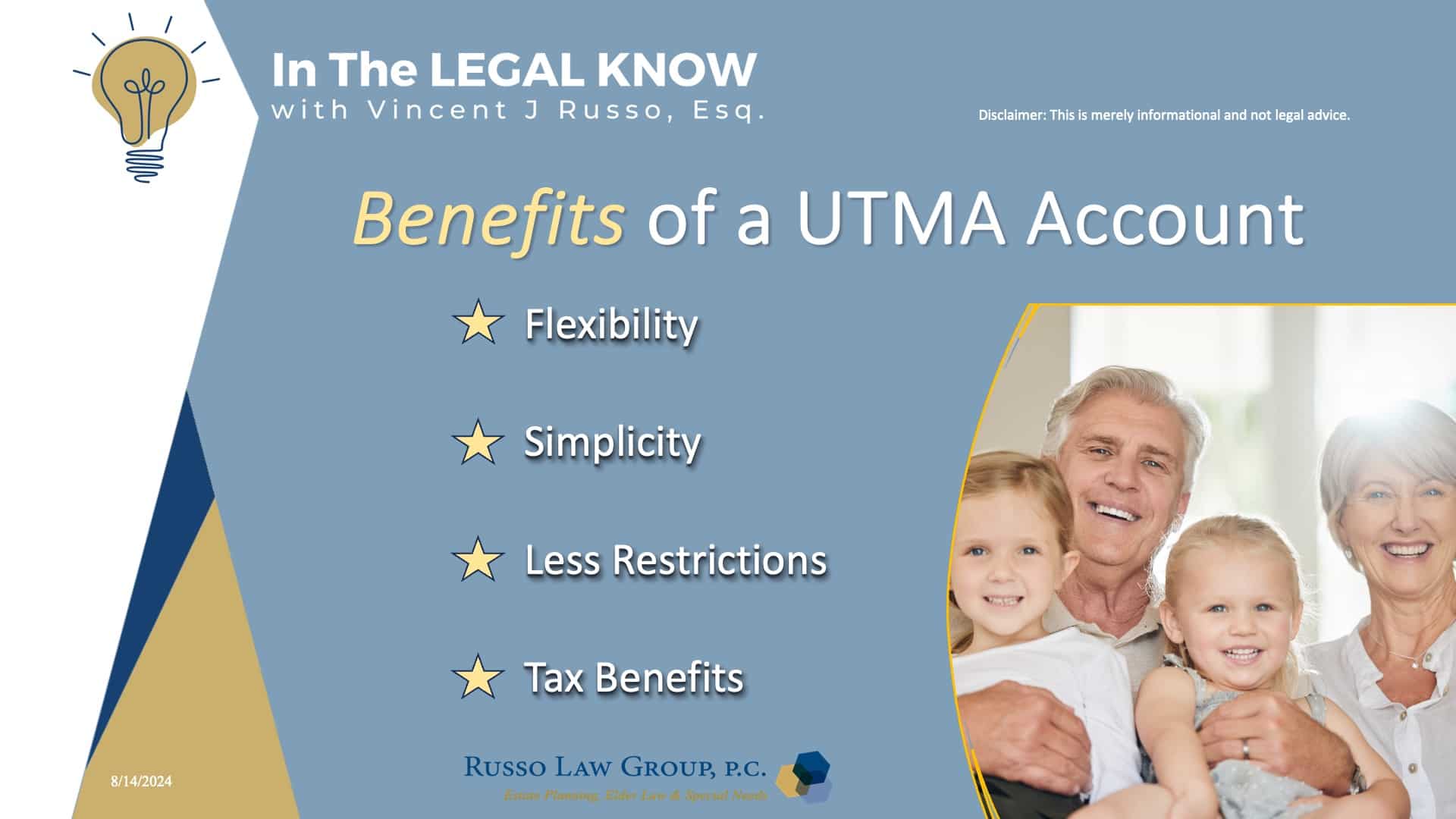

Benefits of a UTMA Account

UTMA accounts offer several advantages that make them a popular choice for gifting assets to minors. These accounts provide flexibility and simplicity, allowing custodians to manage and use the funds in ways that support the child’s needs.

Additionally, there are some tax benefits that can help maximise the value of the assets held within the account. Below are the key benefits of a UTMA account:

- Flexibility: Custodians can use the funds for a wide range of expenses that benefit the minor.

- Simplicity: UTMA accounts are easier to set up than formal trusts.

- Fewer Restrictions: There are no contribution limits or withdrawal restrictions.

- Tax Benefits: The account offers potential tax advantages on investment income. For a child with no earned income in 2024:

- Unearned income up to $1,300 is not taxed.

- The next $1,300 is taxed at the child’s tax rate.

- Any amount above $2,600 is taxed at the parents’ tax rate.

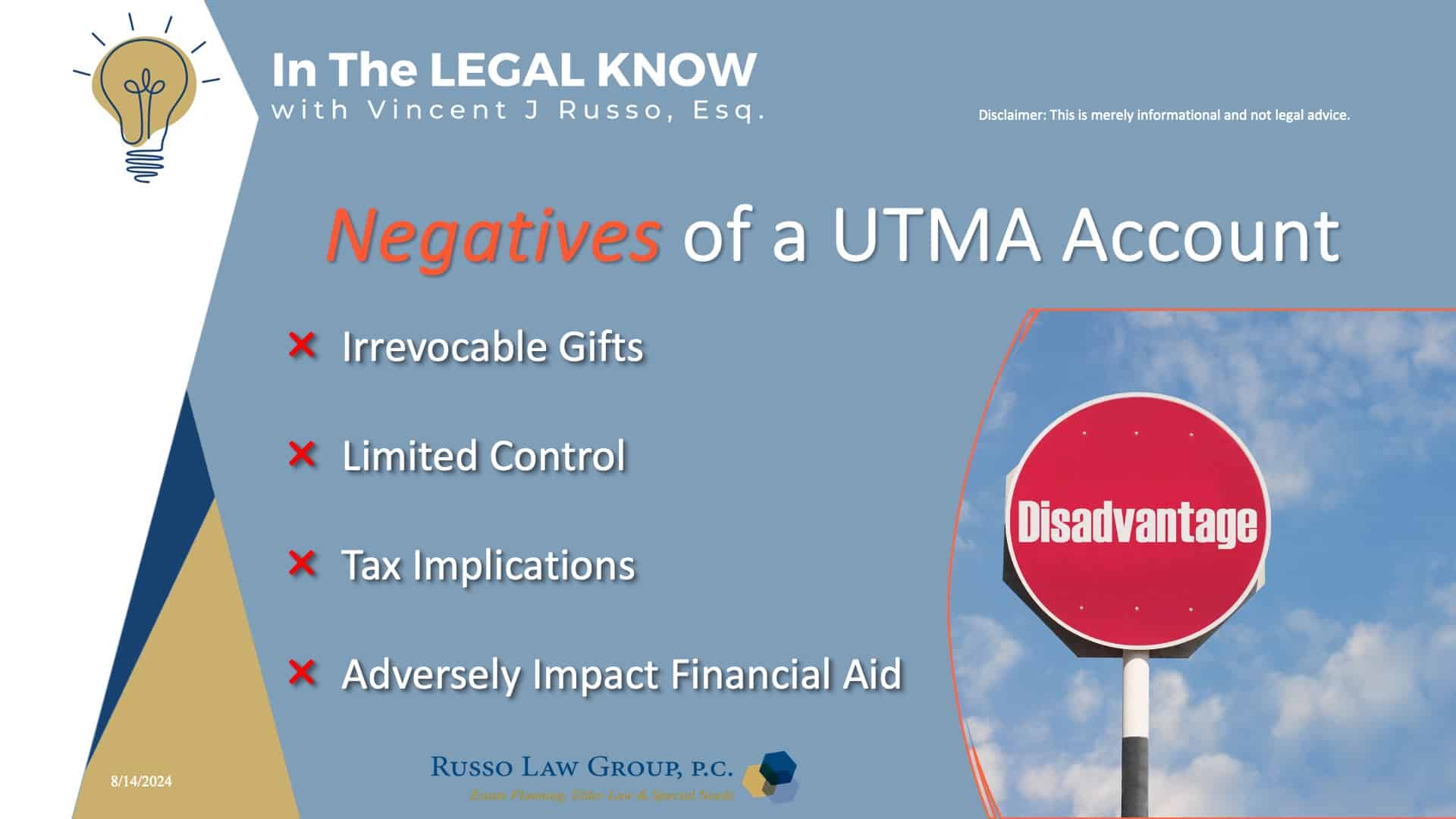

Negatives of a UTMA Account

While UTMA accounts have many benefits, they also come with some drawbacks that you should consider. Understanding these potential negatives can help you decide if a UTMA is the right choice for your situation. Key disadvantages include:

- Irrevocable Gifts: Once you place assets in the UTMA account, you cannot take them back.

- Limited Control: When the child reaches the age of majority, they gain full control of the assets—even if they lack financial experience.

- Tax Implications: The “kiddie tax” may apply, which taxes some of the child’s unearned income at the parents’ tax rate.

- Financial Aid Impact: UTMA accounts count as the child’s assets and may reduce eligibility for need-based financial aid and scholarships.

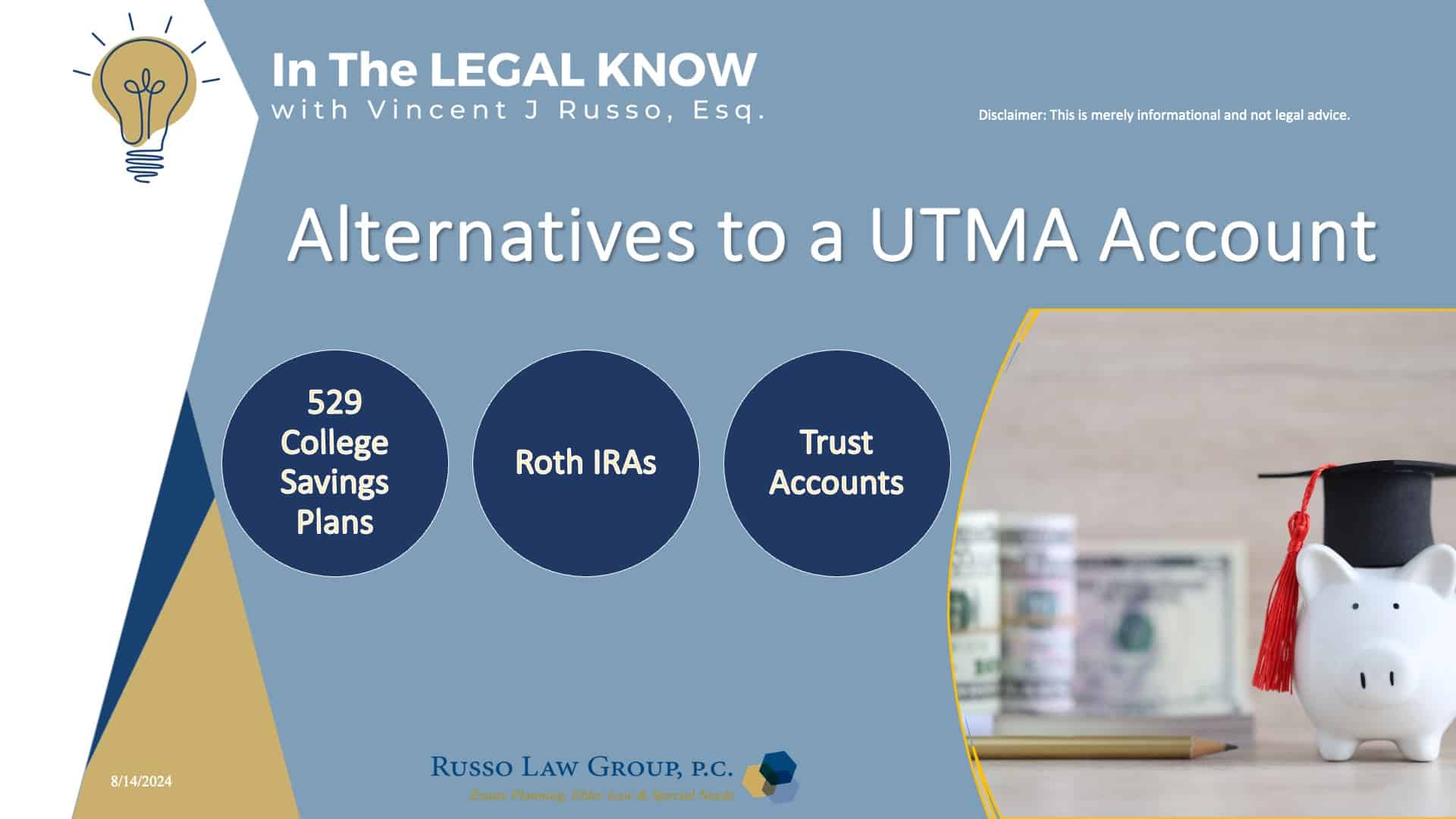

Alternatives to UTMA Accounts

There are several alternatives to UTMA accounts that might better suit your goals, especially if you want more control or tax advantages. Some popular options include:

- 529 College Savings Plans: These offer tax advantages when used for education expenses and typically have less impact on financial aid eligibility.

- Roth IRAs: Suitable for teenagers who have earned income, Roth IRAs allow early saving for retirement with tax benefits.

- Trust Accounts: Trusts provide greater control over how and when assets are distributed, making them ideal for larger sums or when specific conditions must be met.

Bottom Line on UTMA Accounts

The Uniform Transfers to Minors Act (UTMA) lets minors receive gifts and inherit assets without setting up a formal trust. UTMA accounts offer flexibility and simplicity, but when the child reaches the designated age, they gain full control. This transition can affect taxes, financial aid, and asset management.

If your child has special needs, exercise caution. Transferring UTMA assets might affect their eligibility for benefits like Medicaid or Supplemental Security Income.

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 to schedule a consultation and discuss what makes sense for you and your loved ones.

Entradas relacionadas

Comments (0)